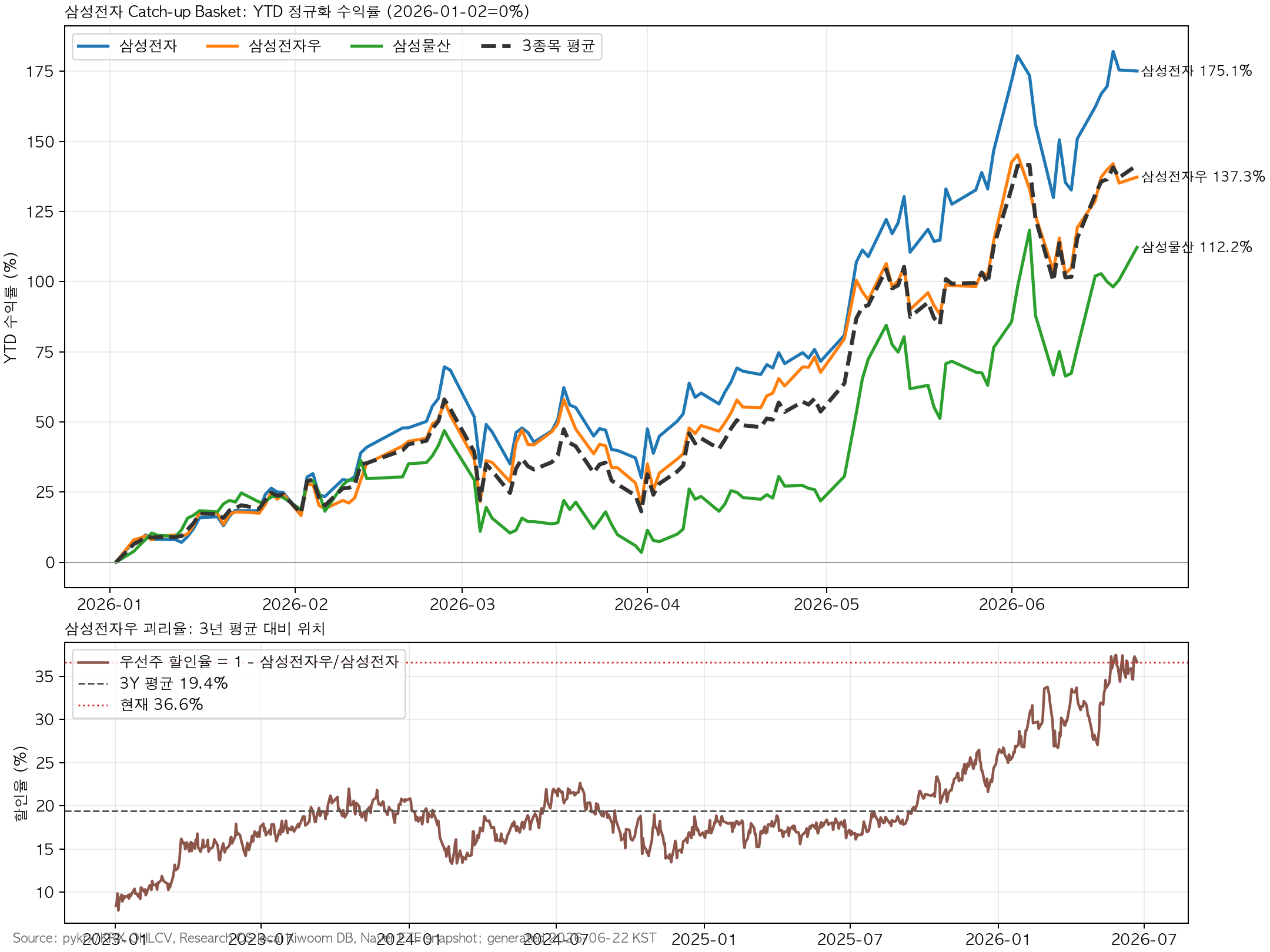

Samsung Electronics preferred is the cleaner catch-up expression. It lagged the common by 37.8 percentage points YTD and traded at a 36.6% discount on 22 June 2026.

The discount is extreme: 36.6% versus a 19.4% three-year average, 18.1% median, +3.11 z-score, and 99.1st percentile.

Samsung C&T is not a one-for-one Samsung Electronics proxy. It is a NAV and affiliate-dividend story.

ETF cap spillover is secondary. A simple redistribution assumption implies only about KRW 24.6bn into Samsung Electronics preferred and KRW 46.0bn into Samsung C&T.

主要データ

Stock

2 Jan Close

22 Jun Close

YTD

Versus Samsung Electronics

Samsung Electronics

KRW 128,500

KRW 353,500

+175.1%

Baseline

Samsung Electronics preferred

KRW 94,400

KRW 224,000

+137.3%

-37.8pp

Samsung C&T

KRW 245,000

KRW 520,000

+112.2%

-62.9pp

Metric

Samsung Electronics

Samsung Electronics Preferred

Samsung C&T

20D return

+18.0%

+19.3%

+24.3%

60D return

+86.3%

+67.0%

+84.7%

Correlation with Samsung Electronics

1.000

0.949

0.779

Beta to Samsung Electronics

1.000

0.912

0.848

優先株ディスカウント

Metric

Value

Preferred/common ratio

63.37%

Current discount

36.63%

Three-year average discount

19.43%

Three-year median discount

18.14%

Current z-score

+3.11

Three-year percentile

99.1%

Preferred/Common Ratio

Implied Preferred Price

Upside

Current 63.4%

KRW 224,000

Baseline

70.0%

KRW 247,450

+10.5%

75.0%

KRW 265,125

+18.4%

80.0%

KRW 282,800

+26.3%

85.0%

KRW 300,475

+34.1%

Samsung C&TのNAV

Samsung C&T is calculated to hold 298,818,100 Samsung Electronics shares. At KRW 353,500, that stake is worth about KRW 105.6tn. Samsung C&T’s estimated market cap is about KRW 84.3tn.

Foreign selling slows, program selling eases, 20-day moving average holds

The key conclusion is that the next Samsung Electronics catch-up alpha is more likely to come from preferred-share discount normalization than from ETF cap spillover.