This note follows the complex risk-off and recovery-trigger framework, KOSPI foreign ownership versus Samsung and SK Hynix, Korea foreign-investor flow analysis and the National Growth Fund / KOSDAQ smart-money map. Those pieces looked at macro gates, KOSPI mega-cap flows and KOSDAQ policy capital. This one asks a simpler question: how healthy is the tape beneath the index?

TL;DR

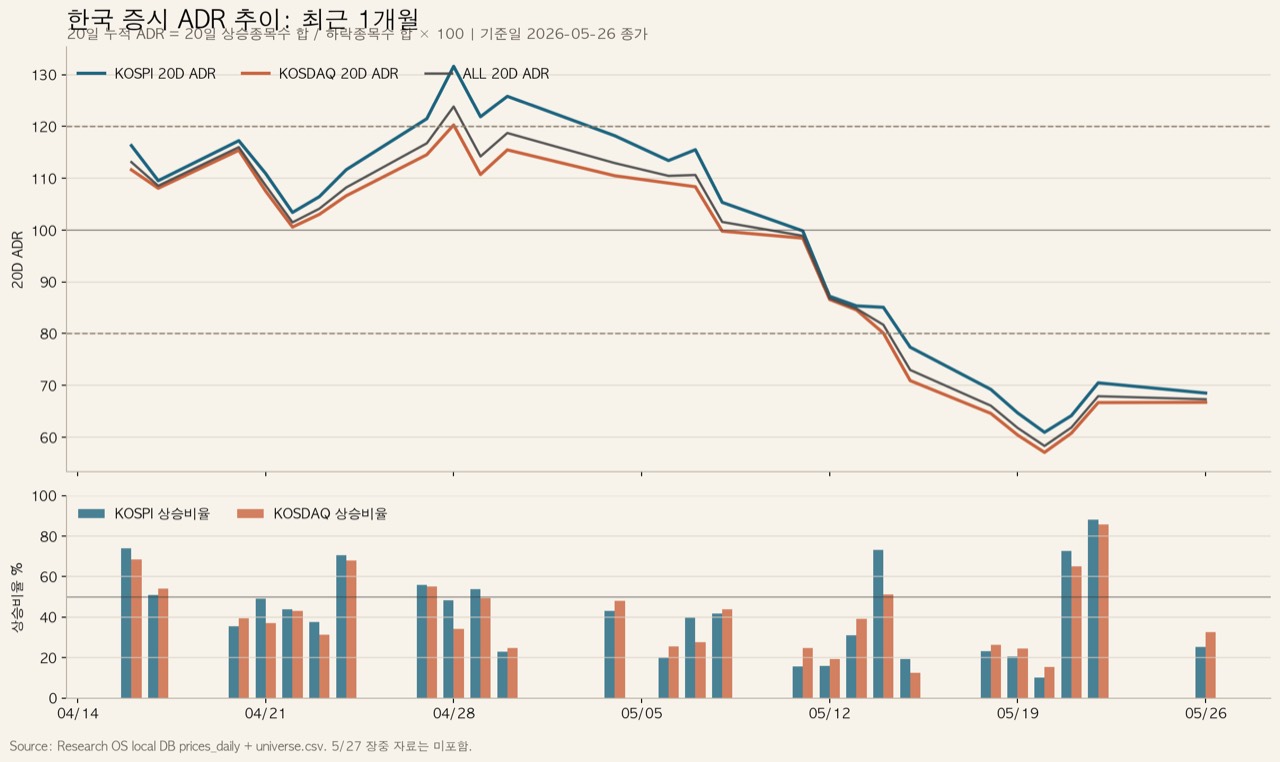

- Korea’s 20-day ADR fell from 113.1 to 67.3 over the last month. KOSPI fell from 116.3 to 68.5 and KOSDAQ from 111.6 to 66.7. The average stock is already in a correction even if the index still holds.

- This is not broad risk-on. It is narrow leadership concentrated in AI infrastructure bottlenecks, MLCC / FC-BGA / SOCAMM / back-end semis, and selected shipbuilding / defense / power names.

- The next trade is not chasing first-line leaders. It is watching for ADR recovery + rising turnover + first foreign / institutional flow into second-line candidates. The local screen points to HPSP, SFA Semicon, Hana Micron, Dongjin Semichem and KMW.

Source: Research OS local DB prices_daily + universe.csv. Data cut is the May 26, 2026 close. May 27 intraday data is not included.

1. What ADR Tells Us

ADR measures market breadth, not index level.

The formula is simple.

Daily ADR = advancing stocks / declining stocks × 100

20D ADR = sum of advancing stocks over 20 sessions / sum of declining stocks over 20 sessions × 100

Advance ratio = advancing stocks / total stocks × 100

An ADR of 100 means advancing and declining stocks are balanced. Below 80, declining stocks are clearly dominating. If ADR sits in the 60s or 70s while the index remains firm, the market is usually being carried by a few large caps or a narrow set of themes.

That is Korea now.

| Market | 2026-04-16 20D ADR | 2026-05-26 20D ADR | Change | Read |

|---|---|---|---|---|

| KOSPI | 116.3 | 68.5 | -47.8p | Large-cap breadth has weakened |

| KOSDAQ | 111.6 | 66.7 | -44.9p | Small/mid-cap breadth has cooled sharply |

| All Korea | 113.1 | 67.3 | -45.8p | The average stock is already weak |

The important point is that this is not only a KOSDAQ problem. KOSPI’s 20-day ADR is also down to 68.5. So the right read is not “KOSDAQ is weak but KOSPI is healthy.” It is this:

Korean market breadth has narrowed, and surviving capital is compressed into AI infrastructure, shipbuilding, defense and a few other leadership pockets.

2. Why the Late-May Bounce Is Not Enough Yet

On May 20, only 333 stocks rose while 2,082 fell. Daily ADR was 16.0 and the advance ratio was 13.5%. That was close to a short-term capitulation session.

The May 21-22 rebound was strong.

| Date | Advancers | Decliners | Daily ADR | 20D ADR | Advance Ratio | Read |

|---|---|---|---|---|---|---|

| 2026-05-20 | 333 | 2,082 | 16.0 | 58.3 | 13.5% | Short-term capitulation |

| 2026-05-21 | 1,695 | 720 | 235.5 | 61.9 | 68.6% | Technical rebound |

| 2026-05-22 | 2,097 | 283 | 742.2 | 67.9 | 86.1% | Strong rebound |

| 2026-05-26 | 749 | 1,660 | 45.1 | 67.3 | 30.2% | Breadth weakened again |

The problem is May 26. After the strong rebound, decliners rose again to 1,660 and the advance ratio fell back to 30.2%.

So the current state is not confirmed breadth expansion. It is a bottoming attempt in breadth that is still being tested.

That links directly to the earlier macro risk-off framework. The condition there was that oil, long rates, the dollar, KRW, Chinese credit and foreign flows needed to stabilize together. The ADR data says that recovery has not yet spread through the market.

3. Current Regime: Narrow Leadership

The current Korean equity regime is Narrow Leadership / Selective Risk-On.

| Item | Read |

|---|---|

| Market breadth | Weak. All-market 20D ADR is 67.3 |

| Leadership | Very strong in AI infrastructure and selected shipbuilding / defense |

| Trading difficulty | High. Stock selection matters more than index direction |

| New exposure | Prefer pullbacks and second-line names over chasing first-line leaders |

| Portfolio stance | Hold relative-strength leaders, replace weak positions, avoid using all cash before breadth recovers |

The mistake is to say “the index is holding, so the whole market is fine.” With ADR in the 60s, most stocks are not fine. The opposite mistake is to say “breadth is bad, so avoid everything.” That is also wrong, because capital is still very active in a narrow set of sectors.

The surviving groups are:

- AI infrastructure bottlenecks: Samsung Electro-Mechanics, Jeju Semiconductor, Daeduck Electronics, Simmtech, Haesung DS, Hana Micron, HPSP

- Memory mega-caps: SK Hynix, Samsung Electronics

- Shipbuilding / defense / nuclear-SMR: HD Hyundai Heavy Industries, Hanwha Ocean, Doosan Fuel Cell

- Power / optical / network: selected power cable, RF and optical names

The market is weak, but leadership is not. That is not a contradiction. When breadth collapses, capital often crowds even harder into the few themes that still work.

4. Where Leadership Actually Was

The last-month leadership list is compressed into AI infrastructure and shipbuilding / defense.

Returns are %, turnover and flows are KRW 100 million units.

| Stock | 1M | 5D | Avg Turnover | Foreign 1M | Institution 1M | Retail 1M | Read |

|---|---|---|---|---|---|---|---|

| Jeju Semiconductor | +173.6 | +28.4 | 3,692.8 | +1,440.8 | +595.8 | -1,962.1 | LPDDR second-order discovery. Hot |

| Samsung Electro-Mechanics | +146.0 | +52.5 | 8,986.4 | -9,036.0 | +4,953.0 | +3,922.2 | MLCC + FC-BGA leader. Institution-led |

| Daeduck Electronics | +81.4 | +20.5 | 1,198.1 | +524.4 | +827.0 | -954.7 | FC-BGA / MLB core name |

| Simmtech | +74.5 | +32.3 | 822.6 | +678.3 | +1,376.0 | -2,070.4 | SOCAMM / substrate core |

| Haesung DS | +72.7 | +19.2 | 297.3 | +132.7 | +656.4 | -53.9 | Heat spreader / substrate option |

| Hana Micron | +48.3 | +5.0 | 1,200.6 | +2,172.5 | +158.3 | +135.8 | Foreign-led back-end recovery |

| HD Hyundai Heavy Industries | +51.0 | +21.1 | 3,642.0 | -5,344.5 | +7,038.2 | -1,987.9 | Institution-led shipbuilding + nuclear option |

| Hanwha Ocean | +2.1 | +16.3 | 2,369.4 | +1,472.3 | +1,393.3 | +6,409.7 | 5D flow improvement, still a laggard |

The key is that not all leadership has the same flow quality.

Samsung Electro-Mechanics rose 146.0% over one month, but foreigners sold KRW 903.6 billion. Institutions and retail absorbed the supply. That fits the SEMCO KRW 100T market-cap note: the AI passive-component re-rating is real, but chasing efficiency has fallen.

Hana Micron, by contrast, rose 48.3% with KRW 217.25 billion of one-month foreign net buying. That is why it looks more like a second-line back-end expansion candidate than an already over-owned first-line leader.

HD Hyundai Heavy Industries was sold by foreigners but bought heavily by institutions. That connects to the HD Hyundai Heavy Industries SMR option analysis: the shipbuilding / engine / SMR story is alive, but the rally is institution-led and price location matters.

5. Is KOSDAQ Weak, Or Selectively Coming Back?

KOSDAQ’s 20D ADR is 66.7. On the surface, that is weak. But it does not mean the whole KOSDAQ should be avoided.

The earlier KOSDAQ smart-money and Pearl Abyss rebound note argued that flows can turn before prices. The ADR data narrows that frame.

What matters is not buying KOSDAQ broadly. It is finding second-line names where turnover is just starting to accelerate, foreign/institutional flows are positive, and the 20-day moving-average extension is still manageable.

The local screen highlights:

| Rank | Stock | Theme | 5D | 20D | 5D Avg Turnover | Turnover Accel. | 20D MA Gap | fi5 | Read |

|---|---|---|---|---|---|---|---|---|---|

| 1 | HPSP | Semi equipment / AI infra | +12.7 | +3.4 | 1,989.2 | 1.28x | +2.9 | +509.3 | Cleanest second-line candidate |

| 2 | SFA Semicon | Back-end | +19.9 | -2.5 | 3,020.5 | 3.41x | +7.4 | +259.1 | Back-end expansion candidate |

| 3 | Hana Micron | Back-end | -1.2 | +16.6 | 1,386.3 | 1.18x | +3.8 | +129.4 | Pullback candidate |

| 4 | Dongjin Semichem | Materials | +5.4 | -4.0 | 642.5 | 1.15x | +3.1 | +447.4 | Materials-flow recovery candidate |

| 5 | KMW | RF / AI-RAN | +11.7 | +20.8 | 259.0 | 1.30x | n/a | +226.8 | AI-RAN event-confirmation candidate |

fi5 is five-day foreign plus institutional net buying. Some local flow fields can be missing or incomplete, so Kiwoom / KRX flow validation is required before stock-level execution.

6. Breadth Expansion Triggers

This is not yet a broad-market buy zone. At an all-market ADR of 67.3, decliners still dominate.

The confirmation checklist is:

| Trigger | Threshold | Meaning |

|---|---|---|

| 20D ADR recovers to 80 | All-market ADR above 80 | Decliner dominance is easing |

| 20D ADR recovers to 100 | All-market ADR above 100 | Advancers and decliners are balanced |

| Daily advance ratio above 55% | 2-3 consecutive sessions | The rebound is not a one-day bounce |

| KOSDAQ turnover rises | Turnover up with more advancers | Small/mid-cap breadth can broaden |

| Foreign selling is absorbed | FX stable and index holds/rises | More absorption than true risk-off |

By sector, the sequence to watch is:

| Sector | Signal | Meaning |

|---|---|---|

| AI infra second-line | HPSP, SFA Semicon, Hana Micron, Dongjin Semichem turnover rising | Internal expansion within semis |

| Optical / RF / AI-RAN | KMW, RFHIC, Oi Solution flow turning | Marvell / NVIDIA AI-RAN linkage |

| FC-BGA / MLB | Daeduck, ISU Petasys, Korea Circuit re-accelerating | Custom ASIC / AI networking confirmation |

| Test sockets / back-end | ISC, Leeno, TSE, Doosan Tesna turnover rising | SOCAMM / ASIC test-infra expansion |

| Shipbuilding / defense second-line | Flows rotate into laggards during leader pullbacks | Rotation within an existing leadership theme |

This links back to the Marvell / Broadcom Korea AI bottleneck preview. If the market is rotating from a single HBM trade into custom ASICs, AI networking, optical links and power integrity, the broad ADR can stay weak while those lower-stack bottlenecks keep attracting turnover.

7. Practical Read

The current Korean tape can be summarized in two lines:

The broad market is weak.

Leadership is not dead.

The action plan must reflect both.

| Action | Condition | Targets |

|---|---|---|

| Hold existing leaders | Relative strength remains intact despite weak ADR | Samsung Electro-Mechanics, Daeduck and other AI infra names |

| Avoid chasing first-line leaders | 20D ADR below 80 | Hot first-line names |

| Watch second-line candidates | Turnover acceleration + positive fi5 + manageable MA gap | HPSP, SFA Semicon, Hana Micron |

| Replace weak positions | Holdings underperform the market and flows are weak | Non-leadership / non-core positions |

| Manage cash | Portfolio concentration is high before breadth recovers | Do not fully deploy cash while breadth is still weak |

Chasing first-line leaders is inefficient here. Samsung Electro-Mechanics, Jeju Semiconductor and Simmtech have already moved sharply. But avoiding all equities because breadth is weak would miss the narrow leadership regime.

The cleaner stance is: hold leaders, watch second-line names, and require ADR above 80 before broadening exposure.

8. Conclusion

Korea is not a dead market. But it is not a broad market either.

As of the May 26, 2026 close, the all-market 20-day ADR is 67.3. KOSPI is 68.5 and KOSDAQ is 66.7. That is a poor backdrop for buying the average stock. At the same time, Samsung Electro-Mechanics, Jeju Semiconductor, Daeduck Electronics, Simmtech, Hana Micron and HD Hyundai Heavy Industries still show strong leadership.

So the regime is narrow leadership, not broad risk-on.

The three checks are:

- Does all-market ADR recover above 80?

- Do KOSDAQ turnover and the number of advancers rise together?

- Do foreign and institutional flows begin to appear in AI-infra second-line names?

Until those conditions improve, chasing first-line leaders is less attractive than observing second-line candidates. If breadth recovers, the market can broaden. If it does not, only a few leaders will survive. The right stance is neither optimism nor pessimism. It is to accept that market breadth is narrow and follow where real turnover and quality flow are appearing.

Appendix. Evidence Classification

[Fact]

- As of May 26, 2026, the all-market 20D ADR was 67.3.

- On April 16, 2026, the all-market 20D ADR was 113.1.

- On May 26, 2026, 749 Korean stocks advanced, 1,660 declined, and daily ADR was 45.1.

- The last-month leadership list includes Samsung Electro-Mechanics, Jeju Semiconductor, Daeduck Electronics, Simmtech, Haesung DS, Hana Micron and HD Hyundai Heavy Industries.

- HPSP, SFA Semicon, Hana Micron and Dongjin Semichem screened relatively well on turnover and flow conditions.

[Inference]

- The current market is narrow leadership, not broad risk-on.

- More important than simple foreign buying is whether a sector can hold price and attract turnover despite foreign selling.

- Within AI infrastructure, rotation can move from SOCAMM / LPDDR into FC-BGA / MLB, back-end, optical and RF.

- Second-line turnover and flow turns have better expected value than chasing first-line leaders after large moves.

[Speculation]

- Marvell earnings may strengthen custom ASIC, optical and AI-RAN themes more than SOCAMM alone.

- Broadcom earnings may re-ignite AI networking, FC-BGA / ABF and high-speed MLB names.

- If ADR recovers above 80, the probability of second-line expansion rises.

[Blocked]

- May 27, 2026 closing ADR is not included in this note.

- Some five-day flow fields may be missing or incomplete in the local DB.

- AI-RAN candidates such as RFHIC and Oi Solution require separate Kiwoom / KRX flow validation before firm stock-level judgment.

Data source: Research OS local DB prices_daily, universe.csv, korea_adr_recent_20260526.csv, korea_leaders_20260415_20260526.csv, second_line_theme_flow_candidates_20260527.csv. Data cut: May 26, 2026 close. This is research commentary, not investment advice.

Disclaimer: For research and information purposes only. Not investment advice. Names cited are for analytical illustration; readers should perform their own due diligence and consult licensed advisors before any investment decision.