Context This is a follow-up to Korea After GTC Taipei: What Happened Overnight?, Korea’s Narrow Jensen Huang Catalyst Market, Korea Foreign-Investor Playbook: KOSPI 168, KOSDAQ 355, and Korea Foreign Investor Flows. Related hubs are the Korea Daily Market Hub and the Korea Stocks for Foreign Investors Hub.

TL;DR

Korea is not in a liquidity-shortage market. Cash near the stock market has expanded sharply. The problem is that the money is not spreading across the whole market. It is flowing narrowly into leadership stocks and the names foreigners still choose to trade.

Foreigners are not simply abandoning Korea. The cleaner read is: sell mega-cap memory, especially Samsung Electronics and SK hynix, and selectively reallocate into KOSDAQ, batteries, robotics, biotech, and selected infrastructure names.

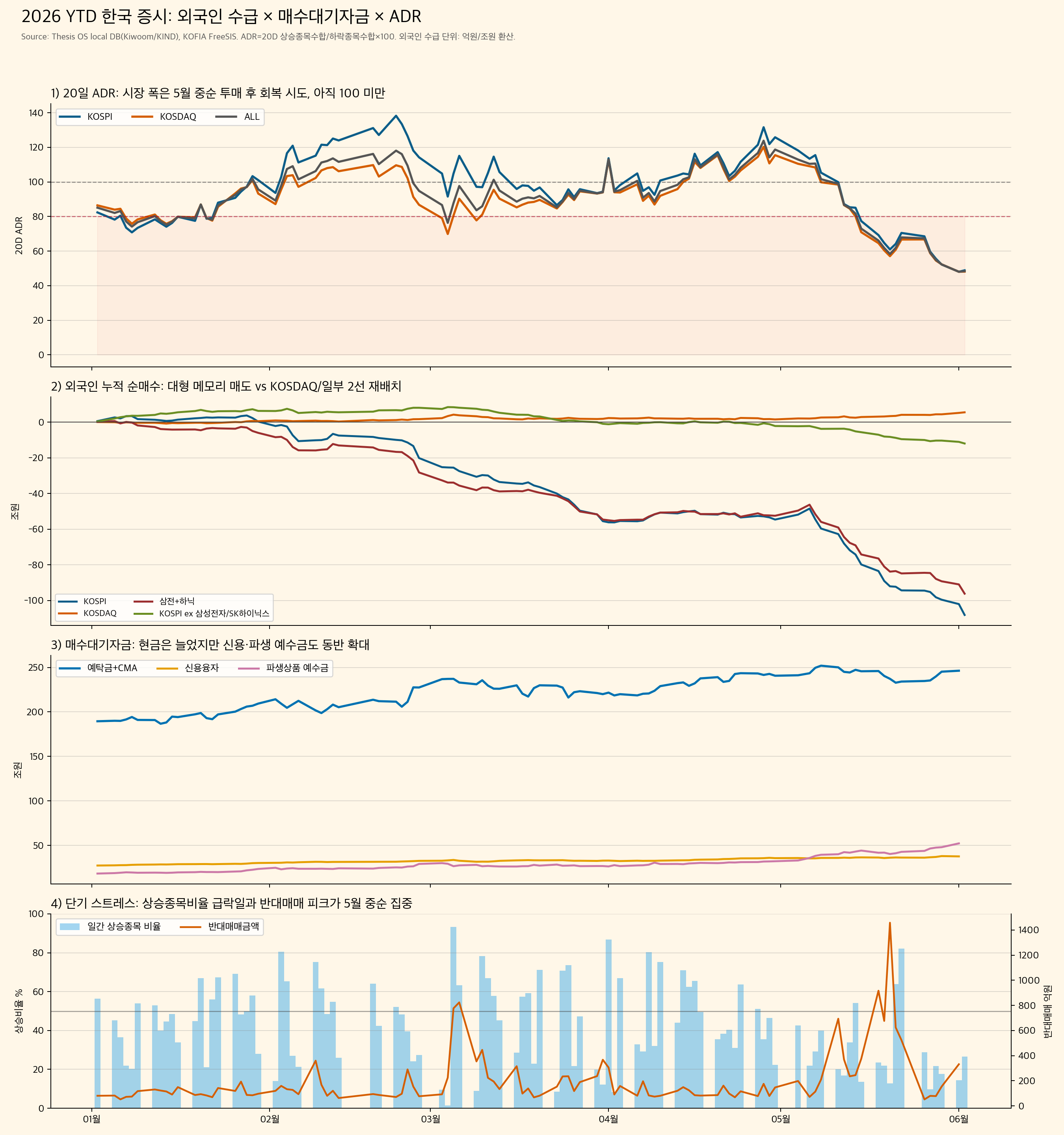

The key warning signal is breadth. As of June 2, 2026, the 20-day ADR was 48.9 for KOSPI, 48.1 for KOSDAQ, and 48.4 for the combined market. That is not a broad risk-on market. It is a selective risk-on market with breadth stress.

1. Core Data

Data basis: Research OS local DB through the June 2, 2026 close for ADR and foreign flows; Korea Financial Investment Association FreeSIS through June 1, 2026 for market-side liquidity. June 3 intraday or close data is not included.

| Item | Date | Value |

|---|---|---|

| KOSPI 20D ADR | 2026-06-02 | 48.9 |

| KOSDAQ 20D ADR | 2026-06-02 | 48.1 |

| Total 20D ADR | 2026-06-02 | 48.4 |

| Advancers / decliners | 2026-06-02 | 693 / 1,741 |

| Investor deposits + CMA | 2026-01-02 → 2026-06-01 | KRW 189.5T → 246.3T |

| Margin loans | 2026-01-02 → 2026-06-01 | KRW 27.4T → 37.7T |

| Derivatives deposits | 2026-01-02 → 2026-06-01 | KRW 18.4T → 52.3T |

| Foreign KOSPI net buying YTD | through 2026-06-02 | KRW -108.1T |

| Foreign KOSDAQ net buying YTD | through 2026-06-02 | KRW +5.5T |

| Samsung Electronics + SK hynix foreign net buying | through 2026-06-02 | KRW -96.1T |

| KOSPI ex Samsung Electronics/SK hynix | through 2026-06-02 | KRW -11.9T |

The three conclusions are simple:

- Liquidity is abundant.

- Foreigners are not leaving Korea wholesale.

- Market breadth is weak.

That is why the market feels strange. The index can hold up, and a few leaders can rally hard, while the average stock keeps weakening.

2. There Is Money, But It Is Narrow

As of June 1, 2026, FreeSIS showed investor deposits of KRW 132.6T, CMA balances of KRW 113.7T, and margin loans of KRW 37.7T. Deposits plus CMA balances were KRW 246.3T. (KOFIA FreeSIS)

| Item | 2026-01-02 | 2026-06-01 | Change | Interpretation |

|---|---|---|---|---|

| Investor deposits | KRW 89.5T | KRW 132.6T | +43.1T / +48.1% | Cash inside brokerage accounts |

| CMA balances | KRW 100.0T | KRW 113.7T | +13.7T / +13.7% | Cash-like parking money |

| Deposits + CMA | KRW 189.5T | KRW 246.3T | +56.8T / +30.0% | Real waiting liquidity |

| Margin loans | KRW 27.4T | KRW 37.7T | +10.3T / +37.4% | Fuel and risk |

| Derivatives deposits | KRW 18.4T | KRW 52.3T | +33.9T / +184.2% | Futures/options/hedging money |

So the right statement is not “there is no money in Korea.” It is:

There is money, but it is not buying the average stock.

This liquidity can cushion pullbacks in leadership names. But it does not guarantee a broad market rally. Because leverage and derivatives deposits have also expanded, this is not pure cash risk-on. It is cash plus leverage plus hedging liquidity.

3. Foreigners Reduced Memory Concentration

KOSPI foreign selling looks enormous, but most of it comes from Samsung Electronics and SK hynix.

| Segment | YTD foreign net buying | May foreign net buying |

|---|---|---|

| KOSPI | KRW -108.1T | KRW -44.9T |

| KOSDAQ | KRW +5.5T | KRW +2.9T |

| Samsung Electronics | KRW -55.8T | KRW -16.0T |

| SK hynix | KRW -40.4T | KRW -20.7T |

| Samsung Electronics + SK hynix | KRW -96.1T | KRW -36.7T |

| KOSPI ex those two | KRW -11.9T | KRW -8.2T |

Foreign ownership data points in the same direction.

| Segment | Start of year | Jun. 2 | YTD change |

|---|---|---|---|

| KOSPI foreign ownership | 36.02% | 39.68% | +3.66pp |

| KOSDAQ foreign ownership | 10.22% | 11.46% | +1.25pp |

| Samsung Electronics foreign ownership | 52.37% | 48.30% | -4.07pp |

| SK hynix foreign ownership | 53.81% | 51.34% | -2.47pp |

Important caveat: the market-wide foreign-ownership figures are local DB estimates, not official full-market KRX aggregates. The direction is still useful: foreign ownership in Samsung Electronics and SK hynix declined, while broad market ownership rose.

4. Where Did the Money Go?

YTD foreign buying leaders include Doosan Enerbility, Celltrion, Samsung SDI, APR, Doosan, Hanwha Ocean, Hyundai Engineering & Construction, Hyundai Rotem, SK Inc., Doosan Robotics, FADU, and Sanil Electric.

May buying leaders were even more revealing: Doosan Robotics, Samsung SDI, FADU, Hyundai E&C, LG Display, Doosan, POSCO Holdings, KT&G, Samsung Fire & Marine, and LG Energy Solution.

The allocation pattern is not “buy all AI infrastructure.” It is much more selective. Foreigners bought selected KOSDAQ AI-storage and semiconductor names, some batteries, robotics, biotech, infrastructure, and shareholder-return defensives, while selling parts of the previously crowded AI-hardware basket.

5. ADR 48 Is the Main Warning

The June 2 20-day ADR was below 50 for both KOSPI and KOSDAQ.

| Market | 20D ADR |

|---|---|

| KOSPI | 48.9 |

| KOSDAQ | 48.1 |

| Total | 48.4 |

This is Selective Risk-On / Breadth Stress.

| Condition | Current read | Meaning |

|---|---|---|

| Foreign flows | KOSPI selling, KOSDAQ selective buying | Not a wholesale Korea exit |

| Liquidity | Waiting money surged | Buying power exists |

| ADR | Below 50 | Breadth is fragile |

| Conclusion | Narrow leadership market | Buy pullbacks only in confirmed leaders |

Practical rules:

- Do not buy broad beta just because liquidity is high.

- Do not interpret foreign selling as a simple Korea exit.

- Watch ADR recovery: 60 is first stabilization, 80 means second-tier spread, 100 means real breadth repair.

- This is a pullback-buying market only for leaders with price strength and still-alive foreign or institutional flows.

6. Final View

Korea is not short of liquidity. But breadth has broken. Foreign selling is being absorbed by local liquidity, yet that money is flowing into a narrow set of leaders and foreign-playbook names.

The next buy signal is not just index strength. It is ADR recovery plus relative strength in the names where foreign reallocation is still visible.

Coverage Health

- ADR and foreign-flow data: Research OS local DB through the June 2, 2026 close.

- Market liquidity: KOFIA FreeSIS through June 1, 2026.

- June 3, 2026 intraday and close data is not reflected.

- Market-wide foreign ownership is a local estimate using foreign market value / estimated total market value, not official full-market KRX aggregation.