Related context This is a follow-up to our H1 2026 AI infrastructure and narrow-market review, Monte Carlo analysis of how hard it was to beat KOSPI, Korea liquidity and collapsing breadth study, and conditions for a KOSDAQ recovery after Samsung Electronics and SK hynix crowding. This time, the semiconductor complex and Samsung Electronics/SK hynix equity proxies are removed to identify what actually led the rest of the market. Related hubs are the Exclusive Analysis Hub and Korea Daily Market Hub.

TL;DR

- As of July 10, 2026, the top KOSPI outperformers outside semiconductors had spread into power grids, construction, retail, financials and holding companies, and energy. The top YTD names were Gaon Cable, Daewoo E&C, Shinsegae, LS ELECTRIC, and Lotte Shopping.

- YTD winners and current leaders are not the same. Among the top KOSPI names, only a much smaller group, including Gaon Cable, Kolmar Korea, GS E&C, S-Oil, KB Financial, GS, Shinhan Financial, and Hana Financial, remained positive over the latest 20 sessions.

- KOSDAQ was far narrower. Only 45 of 138 non-semiconductor names, or 32.6%, were positive YTD. The median YTD return was -12.4% and the median 20-session return was -15.5%, even though the top-ten YTD median was +142.5%.

- The quality of KOSDAQ winners also diverged. FiberPro, Seegene, YG-1, and DKT were supported by earnings or orders. Woori Technology, Solid, and Hyundai Movex combined real business opportunities with thematic premiums. JS Link, Sampyo Cement, Hyundai Bioscience, KMW, and NatureCell were driven more by business-transition, asset-value, clinical, or regulatory options.

1. Universe and methodology

The question is simple: what rose outside semiconductors? A sector-code exclusion alone is not enough because SK Square, Samsung C&T, and Samsung Life remain sensitive to the equity value of Samsung Electronics or SK hynix. This study therefore removes the semiconductor industry, core semiconductor ETF constituents, and major equity-holding proxies.

| Item | KOSPI | KOSDAQ |

|---|---|---|

| Starting universe | Top 200 by market cap | Top 200 by market cap |

| Comparable non-semiconductor companies | 182 | 138 |

| YTD calculation | Adjusted close on Dec. 30, 2025 to adjusted close on July 10, 2026 | Same |

| Recent trend | Latest 20-session adjusted return | Same |

| Main exclusions | ETFs, ETNs, preferred shares, KRX semiconductor names, core semiconductor ETF constituents, Samsung Electronics preferred, SK Square, SK Inc., Samsung C&T, Samsung Life | KRX semiconductor names, semiconductor ETF core/multiple constituents, manually classified semiconductor IP, equipment, and materials names |

| No year-end comparison price | K Bank | MakinaRocks |

Conglomerates such as Doosan and Foosung remain when their primary industry is non-semiconductor, despite partial semiconductor exposure. RFHIC and RF Materials are retained as communications and RF businesses.

Market-cap ranks use the July 10, 2026 Naver Finance KOSPI and KOSDAQ screens. Full results are available as 182-name KOSPI CSV and 138-name KOSDAQ CSV.

2. KOSPI: leadership spread into five non-semiconductor lanes

The top 30 non-semiconductor names include five construction companies, three retailers, and four electrical-equipment or cable names. Financial and holding companies, energy, defense, telecom, and batteries also appear. “Financial and holding companies” is an analytical grouping that combines banks, brokers, insurers, and holding companies rather than one exchange industry code. The full KOSPI non-semiconductor universe was not extremely narrow, with 63.2% positive YTD, but the largest excess returns were concentrated in a handful of sectors.

| Rank | Company | Market-cap rank | YTD | Latest 20D |

|---|---|---|---|---|

| 1 | Gaon Cable | 108 | +455.8% | +81.7% |

| 2 | Daewoo E&C | 81 | +356.8% | -20.1% |

| 3 | Shinsegae | 90 | +154.7% | -9.5% |

| 4 | LS ELECTRIC | 23 | +120.1% | -9.0% |

| 5 | Lotte Shopping | 107 | +114.2% | -20.6% |

| 6 | SK Eternix | 194 | +107.0% | -0.3% |

| 7 | LG Electronics | 25 | +98.5% | -19.1% |

| 8 | Mirae Asset Life Insurance | 148 | +95.3% | -35.3% |

| 9 | SK Networks | 181 | +89.8% | -34.0% |

| 10 | Hyundai Department Store | 119 | +88.6% | -5.8% |

| 11 | Samsung E&A | 76 | +83.4% | -7.4% |

| 12 | Foosung | 193 | +82.5% | -27.7% |

| 13 | Mirae Asset Securities | 31 | +81.5% | -19.3% |

| 14 | LIG Defense & Aerospace | 47 | +77.9% | -3.0% |

| 15 | Doosan | 34 | +77.0% | -27.1% |

| 16 | OCI Holdings | 117 | +71.7% | -34.1% |

| 17 | Kolmar Korea | 147 | +71.5% | +23.3% |

| 18 | Hyundai G.F. Holdings | 162 | +68.3% | +1.6% |

| 19 | SK Telecom | 40 | +65.8% | -13.9% |

| 20 | LS Corp. | 65 | +64.6% | -14.9% |

| 21 | Hyosung Heavy Industries | 27 | +64.2% | -13.4% |

| 22 | Doosan Fuel Cell | 125 | +63.1% | -35.6% |

| 23 | APR | 55 | +62.3% | -4.8% |

| 24 | GS E&C | 139 | +61.7% | +10.6% |

| 25 | Samsung SDI | 21 | +61.0% | -19.5% |

| 26 | S-Oil | 52 | +59.2% | +18.6% |

| 27 | Hyundai Motor | 6 | +54.3% | -24.6% |

| 28 | DL E&C | 151 | +53.8% | -14.3% |

| 29 | Hyundai E&C | 61 | +52.9% | -31.9% |

| 30 | NH Investment & Securities | 62 | +49.8% | -0.5% |

| 31 | Samsung Securities | 67 | +48.5% | -5.7% |

| 32 | KB Financial | 9 | +47.9% | +14.4% |

| 33 | Korea Investment Holdings | 59 | +47.8% | -0.6% |

| 34 | DN Automotive | 167 | +46.9% | -11.0% |

| 35 | Sanil Electric | 92 | +45.3% | -18.3% |

| 36 | Hanwha Life | 111 | +42.9% | -6.4% |

| 37 | GS Holdings | 79 | +42.5% | +10.6% |

| 38 | Shinhan Financial | 14 | +42.0% | +9.6% |

| 39 | Douzone Bizon | 121 | +40.2% | 0.0% |

| 40 | Hana Financial | 20 | +36.6% | +6.2% |

Gaon Cable requires an adjusted-price caveat

Gaon Cable went ex-rights for a bonus issue on June 30, 2026. The company allotted 0.8 new shares per common share, and the exchange set the reference price at KRW190,600. Ex-rights report

Its adjusted-price YTD return is +455.8%, while a simple raw-close comparison produces +208.9%. Adjusted prices are appropriate for long-horizon comparisons, but readers should understand why the number differs from a basic chart-screen calculation.

3. Which KOSPI YTD winners are still leading?

Only nine of the top 40 remained positive over the latest 20 sessions.

| Company | YTD | Latest 20D | Current read |

|---|---|---|---|

| Gaon Cable | +455.8% | +81.7% | The strongest grid/cable momentum, with unusually high corporate-action and price volatility |

| Kolmar Korea | +71.5% | +23.3% | Export consumer and earnings momentum remain intact |

| S-Oil | +59.2% | +18.6% | Refining-cycle and margin expectations continue to support returns |

| KB Financial | +47.9% | +14.4% | Large-cap financial and shareholder-return leadership remains intact |

| GS E&C | +61.7% | +10.6% | Relatively strong recent price action among construction rerating candidates |

| GS Holdings | +42.5% | +10.6% | Refining, energy asset value, and holding-company discount compression |

| Shinhan Financial | +42.0% | +9.6% | Shows that financial leadership is broader than one bank |

| Hana Financial | +36.6% | +6.2% | A key test of the banking rally’s durability |

| Hyundai G.F. Holdings | +68.3% | +1.6% | Retail/holding-company rerating survives, but momentum has slowed |

Daewoo E&C, Mirae Asset Life, SK Networks, OCI Holdings, Doosan Fuel Cell, and Hyundai E&C were YTD winners but fell more than 20% over the latest 20 sessions. Their YTD rank increasingly describes past flows rather than current leadership.

4. KOSDAQ: bigger winners, weaker market

Optical communications, telecom equipment, nuclear and power, electronic components, and healthcare dominated the non-semiconductor KOSDAQ leaders. Yet a small set of spectacular winners coexisted with a broadly weak market.

| Rank | Company | Market-cap rank | YTD | Latest 20D |

|---|---|---|---|---|

| 1 | Taihan Fiberoptics | 46 | +491.0% | -33.8% |

| 2 | YG-1 | 94 | +324.5% | +41.2% |

| 3 | DKT | 197 | +223.6% | +4.7% |

| 4 | Woori Technology | 48 | +208.0% | -36.2% |

| 5 | Samji Electronics | 137 | +145.3% | -13.0% |

| 6 | Sung Ho Electronics | 58 | +139.7% | -52.5% |

| 7 | RF Materials | 184 | +132.0% | -21.6% |

| 8 | JS Link | 67 | +118.2% | +18.2% |

| 9 | Seojin System | 28 | +87.2% | -37.0% |

| 10 | Vitzrocell | 64 | +76.5% | -33.7% |

| 11 | Sampyo Cement | 85 | +65.5% | -28.4% |

| 12 | InBody | 113 | +60.3% | +18.4% |

| 13 | RFHIC | 65 | +59.6% | -32.3% |

| 14 | Sphere | 74 | +48.4% | -40.6% |

| 15 | Hyundai Bioscience | 117 | +46.2% | -18.5% |

| 16 | Solid | 127 | +44.9% | -16.5% |

| 17 | Aju IB Investment | 176 | +39.7% | -50.9% |

| 18 | Mirae Asset Venture Investment | 87 | +33.7% | -57.1% |

| 19 | Cheryong Electric | 112 | +28.8% | -12.7% |

| 20 | Daejoo Electronic Materials | 68 | +28.5% | -32.5% |

| 21 | Satrec Initiative | 81 | +28.4% | -25.2% |

| 22 | FiberPro | 196 | +25.9% | -11.2% |

| 23 | Cosmecca Korea | 86 | +24.6% | +20.6% |

| 24 | Hyundai Movex | 35 | +23.7% | -40.6% |

| 25 | KMW | 105 | +21.9% | -36.5% |

| 26 | Seegene | 61 | +21.8% | +3.4% |

| 27 | Intellian Technologies | 102 | +21.8% | -30.8% |

| 28 | L&C Bio | 45 | +19.0% | -5.5% |

| 29 | EcoPro HN | 139 | +16.4% | -0.7% |

| 30 | NatureCell | 57 | +15.6% | -21.3% |

Pearl Abyss ranked 48th in this non-semiconductor group, with a -0.9% YTD return and -10.0% over the latest 20 sessions.

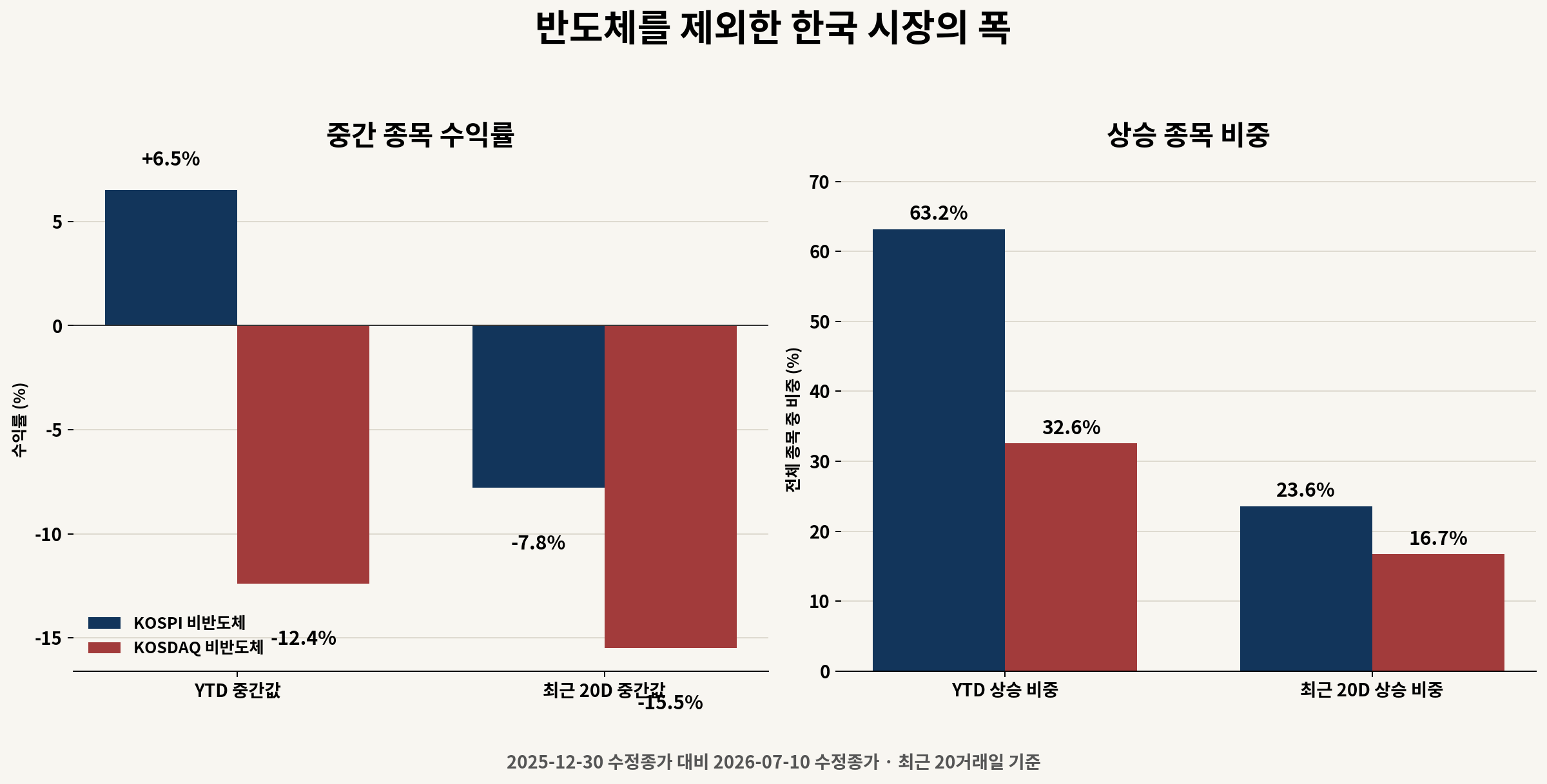

5. KOSPI versus KOSDAQ breadth

| Metric | KOSPI non-semiconductor | KOSDAQ non-semiconductor |

|---|---|---|

| Comparable names | 182 | 138 |

| Median YTD return | +6.5% | -12.4% |

| YTD gainers | 115 | 45 |

| YTD positive share | 63.2% | 32.6% |

| Median latest-20D return | -7.8% | -15.5% |

| Latest-20D gainers | 43 | 23 |

| Latest-20D positive share | 23.6% | 16.7% |

| Top-ten median YTD return | +110.6% | +142.5% |

This is the central result. KOSDAQ’s top ten outperformed KOSPI’s top ten, but the KOSDAQ median stock fell 12.4% YTD. Winner magnitude was greater, and the rest of the market was weaker.

The statement that liquidity rotated beyond semiconductors is partly true for KOSPI, where 63.2% of non-semiconductor names were positive YTD. It is not yet true for KOSDAQ as a whole, where only 32.6% were positive.

6. Why did the selected KOSDAQ winners rise?

The following 13 names are selected cases used to distinguish the quality of each rally, not a fundamental review of every top-30 name. Several high-return companies, including Taihan Fiberoptics, Sung Ho Electronics, and RF Materials, are not classified in this section.

6-1. Earnings and orders supported the move

| Company | YTD | Verified change | First rejection |

|---|---|---|---|

| YG-1 | +324.5% | 1Q26 revenue KRW207.8bn, operating profit KRW38.8bn, 18.7% margin; recovery in global cutting-tool demand and mix | Sharp 2Q margin normalization and weaker orders |

| DKT | +223.6% | Expansion from OLED components into ESS BMS, battery packs, automotive OLED, and robot charging modules; 2026 estimates revised higher | North American ESS expansion fails to convert to revenue |

| FiberPro | +25.9% | Defense and space FOG/IMU/INS demand connected to earnings and orders; 1Q revenue about KRW14.3bn, operating profit about KRW4.8bn | Backlog conversion delay or one-off margin conclusion |

| Seegene | +21.8% | 1Q26 revenue KRW129.1bn and operating profit KRW23.6bn; non-respiratory syndromic products plus dividend and buyback cancellation | Non-respiratory growth slows and core earnings stall |

YG-1 has the fastest earnings improvement and the largest price move, but a good company and a good entry price are separate questions. DKT’s logic is a 1Q earnings beat combined with ESS BMS, auto, and robotics revenue. DKT 1Q and estimate revision

6-2. Real business opportunity mixed with thematic premium

| Company | YTD | Business evidence | Remaining test |

|---|---|---|---|

| Woori Technology | +208.0% | Nuclear MMIS/DCS history, Shin Hanul 3 and 4 revenue, about KRW9.2bn KHNP order | Speed of conversion from orders to profit after a 1Q operating loss |

| Solid | +44.9% | North American DAS orders, Poland and Saudi expansion, 6G project | Whether AI-RAN becomes direct, repeatable revenue |

| Hyundai Movex | +23.7% | Logistics automation, AMR, unmanned warehouses, and KRW55.9bn Kolmar logistics-center order | Conversion from 1Q operating loss to profitable backlog execution |

| Samji Electronics | +145.3% | 1Q consolidated revenue KRW1.904tn and operating profit KRW334.2bn; electronics distribution generated 97.9% of operating profit | Whether the distribution margin spike repeats in 2Q |

Samji requires separate treatment. Its 2026 first-quarter filing shows KRW1.904tn of revenue and KRW334.2bn of operating profit. Electronics distribution contributed KRW327.1bn, or 97.9% of operating profit. The segment margin rose from roughly 2.5% a year earlier to 18.2%.

Inventory and distribution-margin benefits from higher semiconductor prices are a plausible explanation, but the company did not fully explain the jump. The key question is whether a similar margin repeats in 2Q.

Solid and KMW also received an AI-RAN premium after Samsung Electronics announced an AI-native network collaboration with NVIDIA. Company-specific direct orders still require separate confirmation. Samsung AI-RAN announcement

6-3. Option value led current fundamentals

| Company | YTD | Option driving price | Main risk |

|---|---|---|---|

| JS Link | +118.2% | Rare-earth permanent-magnet transition, Malaysia facility, potential US supply-chain entry | Loss-making legacy business; certification and mass-production revenue unverified |

| Sampyo Cement | +65.5% | Mixed-use redevelopment of the Sampyo Group’s Seongsu ready-mix site | No confirmed direct attribution of development profit to Sampyo Cement |

| Hyundai Bioscience | +46.2% | Xafty dengue phase 2/3 in Vietnam, emergency-use and US trial options | Binary clinical and regulatory outcome |

| KMW | +21.9% | AI-RAN and Massive MIMO supply-chain expectation | Direct AI-RAN orders and 1Q profit recovery unverified |

| NatureCell | +15.6% | First-instance court win regarding the JointStem approval rejection and potential FDA path | The ruling is not product approval; review and appeal risks remain |

These ideas are not necessarily wrong. Their value, however, changes discretely with a contract, certification, trial, approval, or asset-value attribution. They should not be sized or assessed like recurring-earnings businesses.

7. Only six top-30 KOSDAQ names remained positive over 20 sessions

| Rank | Company | YTD | Latest 20D | Current status |

|---|---|---|---|---|

| 1 | YG-1 | +324.5% | +41.2% | Earnings and momentum are strong, but expectations are highest |

| 2 | DKT | +223.6% | +4.7% | New-business thesis survives, though momentum slowed |

| 3 | JS Link | +118.2% | +18.2% | Business-transition option still leads price |

| 4 | InBody | +60.3% | +18.4% | Healthcare quality relative strength remains intact |

| 5 | Cosmecca Korea | +24.6% | +20.6% | Export cosmetics and ODM catch-up strength |

| 6 | Seegene | +21.8% | +3.4% | Earnings and capital returns are being priced gradually |

Taihan Fiberoptics, Woori Technology, Seojin System, and RFHIC were major YTD winners but fell more than 30% over the latest 20 sessions. This is why a YTD table cannot be read as a current-leadership table.

8. Three distinctions investors need

First, sector breadth is not stock breadth. KOSPI produced new leadership lanes in grids, construction, retail, financials, and refining, but only a few names remained strong recently.

Second, YTD return is not current relative strength. Daewoo E&C gained 356.8% YTD but lost 20.1% over 20 sessions. Taihan Fiberoptics gained 491.0% YTD but lost 33.8% recently. A year-to-date winner may be evidence of an earlier flow, not a current entry candidate.

Third, recurring earnings and discrete options require different treatment. FiberPro, Seegene, and DKT can be tested against quarterly revenue, profit, and orders. Clinical, approval, business-transition, and real-estate options can pay off dramatically but are harder to verify along the way.

9. Research-priority funnel

This is an idea-triage screen, not a final recommendation.

| Tier | Candidates | Why | Next evidence |

|---|---|---|---|

| A, immediate deeper work | Kolmar Korea, S-Oil, KB Financial, FiberPro, Seegene | Price action or earnings and order evidence is sufficiently clear to justify earlier follow-up work | 2Q earnings, estimate revisions, detailed foreign and institutional flows |

| B, price and expectations gated | Gaon Cable, YG-1, DKT, GS E&C | Current trend is strong, but price gains and expectations are high | Corporate-action adjustment, repeat orders, 2Q margin |

| B, event confirmation | Woori Technology, Solid, Hyundai Movex, Samji Electronics | Real operating links exist, but profit conversion or repeatability remains open | New orders, 2Q margin, exit from losses |

| C, option watch | JS Link, Sampyo Cement, Hyundai Bioscience, KMW, NatureCell | Upside can be large, but depends on discrete events | Contract, certification, clinical, regulatory, or profit-attribution disclosure |

Tier A does not mean “buy now.” It means the company deserves deeper earnings and valuation work before the other candidates. For names such as Gaon Cable and YG-1, company quality and entry-price quality must be separated.

10. Limits and falsifiers

- This is a cross-sectional study that starts with the top 200 market-cap names in each market, not the full Korean listed universe.

- Semiconductor exclusions combine KRX sectors, ETF inclusion, and manual classification. Conglomerates such as Doosan and Foosung remain despite partial semiconductor exposure.

- Adjusted prices include corporate actions. Gaon Cable requires a separate raw-price interpretation.

- The 20-session return is only a simple trend proxy. Current leadership also requires investor-flow, trading-value, and estimate-revision evidence.

- No new company disclosure was identified that fully explains YG-1’s late-June/early-July surge or KMW’s July 10 move. Price momentum should not be mistaken for new fundamentals.

The narrow-market diagnosis should be revised if more than half of KOSDAQ non-semiconductor names turn positive YTD and the median 20-session return turns positive. Conversely, if the KOSPI non-semiconductor 20-session positive share falls further and financial, refining, and construction relative strength breaks, the apparent rotation outside semiconductors was only temporary.

Conclusion

Removing semiconductors does not leave an empty market. KOSPI clearly produced leadership in grids, construction, retail, financials, holding companies, and refining. Yet few names retained momentum through the latest 20 sessions.

KOSDAQ is even clearer. Its top ten rose more than KOSPI’s top ten, while two-thirds of the non-semiconductor universe remained below year-end levels. This is not a broad KOSDAQ rerating. It is a market where capital concentrated in a small set of stocks, themes, and event groups.

The next step is not to chase the YTD winner. It is to ask, in order: Is the stock still strong? Can earnings repeat? Do orders convert to revenue? How much expectation is already in the price? Leadership broadened outside semiconductors, but the list of names worth immediate deeper work remains narrow.

Data as of July 10, 2026. Returns use adjusted closing prices and are rounded to one decimal place. This article is a market-structure study for informational purposes, not a recommendation to buy or sell any security.