Context This is a follow-up to Who Owns Rejuran? PharmaResearch and Korea’s Skin-Booster Platform and PharmaResearch: The PDRN Pioneer Behind Rejuran. Those notes explained the PN/PDRN platform and Rejuran brand. This note asks why the market cut the multiple after 1Q26, and whether Rejuran Cosmetics’ U.S. sell-through can reopen the re-rating path. The broader map sits in the Olive Young, PharmaResearch and K-Beauty Hub.

Key Visuals

TL;DR

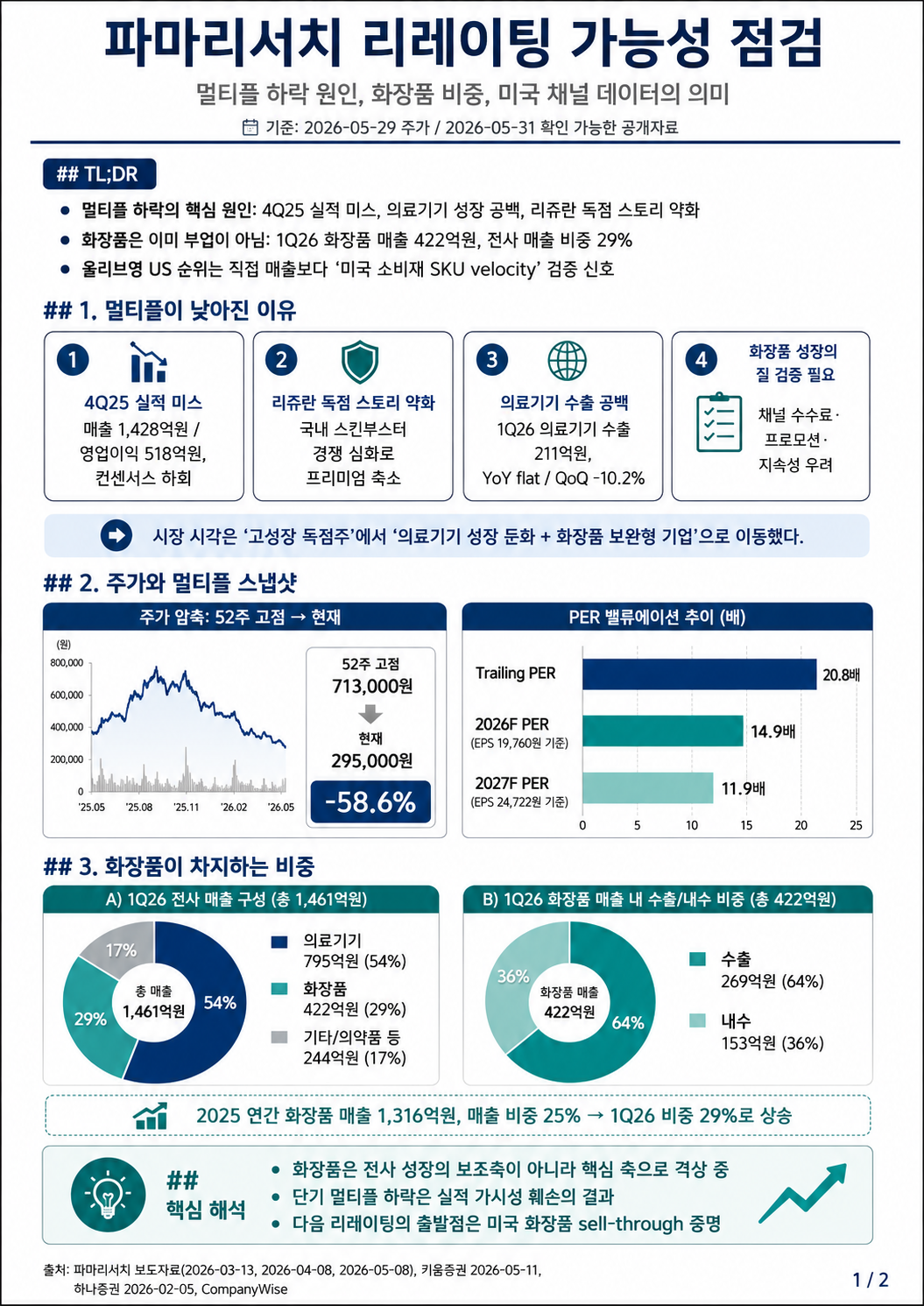

PharmaResearch’s multiple compression is not just a flow correction. It reflects four issues at once: the 4Q25 earnings miss, a pause in medical-device export growth, tougher domestic skin-booster competition and skepticism about the durability of cosmetics revenue.

But cosmetics is no longer a side business. In 1Q26, PharmaResearch reported cosmetics revenue of KRW 42.2B, roughly 29% of consolidated revenue, with cosmetics exports of KRW 26.9B. Rejuran Cosmetics is already the company’s second growth engine. (PharmaResearch 1Q26 release)

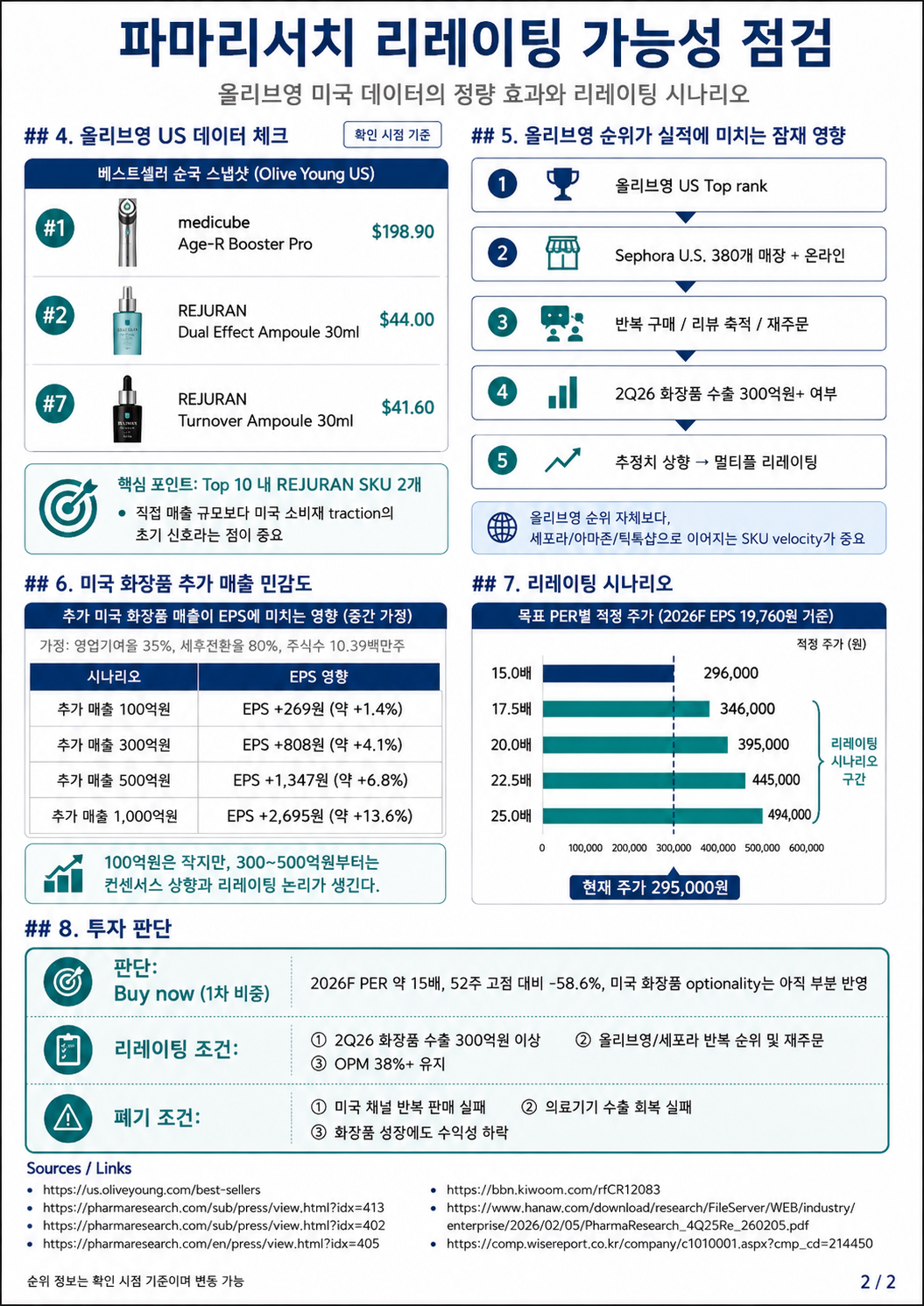

The newest signal is Olive Young U.S. As checked on May 31, 2026, Olive Young U.S. says its best-seller list is updated daily based on sales data. REJURAN Dual Effect Ampoule ranked #2, while REJURAN Turnover Ampoule ranked #7. This is not yet proof of large revenue. It is an early signal that U.S. consumers are buying the Rejuran skincare SKUs. (Olive Young US Best Sellers)

My conclusion is Buy now, but only a first tranche. At KRW 295,000, the stock trades around 14.9x 2026F EPS using Kiwoom’s KRW 19,760 estimate. That already prices in much of the medical-device slowdown concern. A larger position should wait for 2Q26 cosmetics exports above KRW 30B, U.S. channel re-orders and consolidated OPM above 38%.

1. Why the Multiple Fell

The key is reclassification.

PharmaResearch used to be priced as a Rejuran medical-device monopoly growth stock. It created the Korean skin-booster category, had strong PN/PDRN brand recognition and a clinic network. That kind of company can receive 25x or 30x multiples when growth visibility stays clean.

Since late 2025, the market has seen a more complicated story.

| Compression Driver | Why It Matters |

|---|---|

| 4Q25 earnings miss | When a high-multiple growth stock needs complicated explanations, the discount rate rises. |

| Medical-device export pause | 1Q26 medical-device exports were KRW 21.1B, flat YoY and down QoQ. The core segment paused. |

| Domestic skin-booster competition | Rejuran still leads, but the category-monopoly narrative weakened. |

| Cosmetics quality discount | Cosmetics revenue carries channel fees, promotion, inventory and hit-SKU durability risk. |

Kiwoom described 1Q26 as a quarter where cosmetics more than offset the medical-device gap, and its report showed 2026F EPS of KRW 19,760 and 2027F EPS of KRW 24,722. (Kiwoom report)

The multiple fall is therefore not random. It is the market moving PharmaResearch from “medical-device monopoly” to “hybrid beauty-healthcare platform where cosmetics must prove durability.”

2. Cosmetics Is No Longer a Side Business

1Q26 consolidated revenue was KRW 146.1B, operating profit was KRW 57.3B, and OPM was 39.2%. The company called it a record quarterly result. (PharmaResearch 1Q26 release)

| Item | 1Q26 Revenue | Mix |

|---|---|---|

| Consolidated revenue | KRW 146.1B | 100.0% |

| Medical devices | KRW 79.5B | 54.4% |

| Cosmetics | KRW 42.2B | 28.9% |

| Cosmetics exports | KRW 26.9B | 18.4% of total, 63.7% of cosmetics |

| Domestic cosmetics | KRW 15.3B | 10.5% of total, 36.3% of cosmetics |

The math is simple.

Cosmetics mix = 42.2 / 146.1 = 28.9%

Cosmetics export mix = 26.9 / 42.2 = 63.7%

Cosmetics exports / total revenue = 26.9 / 146.1 = 18.4%

That is large enough to change the investment frame. PharmaResearch is not just a medical-device company selling some cosmetics. It is trying to convert Rejuran’s procedure brand equity into derma-cosmetic SKUs.

If that works, the multiple logic changes. Medical-device revenue is tied to clinic channels, procedure demand and regulatory expansion. Cosmetics revenue can scale through Olive Young, Sephora, Amazon and TikTok Shop. The margin and repeat-purchase quality still need proof.

3. Why Olive Young U.S. Matters

Olive Young U.S. says its best-seller list is “updated daily based on sales data.” As checked on May 31, 2026, medicube Age-R Booster Pro ranked #1, REJURAN Dual Effect Ampoule ranked #2 and REJURAN Turnover Ampoule ranked #7. (Olive Young US Best Sellers)

| Rank | Brand / Product | Price |

|---|---|---|

| #1 | medicube Age-R Booster Pro | $198.90 |

| #2 | REJURAN Dual Effect Ampoule 30ml | $44.00 |

| #7 | REJURAN Turnover Ampoule 30ml | $41.60 |

The important part is not only the #2 rank. It is that two REJURAN SKUs were simultaneously in the Top 10. That is stronger than a single promotion-driven spike.

But the interpretation must stay conservative. Olive Young U.S. will not immediately change consolidated earnings by itself. The key question is whether it validates SKU velocity in a U.S. consumer channel.

Olive Young U.S. Top 10

→ Sephora U.S. online + about 380 stores

→ repeat purchases / reviews / re-orders

→ 2Q26 cosmetics exports above KRW 30B

→ estimate revisions

→ multiple re-rating

PharmaResearch announced in March 2026 that Rejuran Cosmetics had entered Sephora U.S. online and about 380 physical stores. Its April English release said the LA pop-up drew more than 5,000 visitors and that Turnover Ampoule and Dual Effect Ampoule saw consistent sell-through during the event. (Sephora launch, LA pop-up)

4. Small Direct EPS Impact, Larger Multiple Impact

The direct earnings impact of an Olive Young U.S. ranking is still small. The re-rating impact can be larger if U.S. cosmetics sales accumulate into estimate revisions.

Assumptions:

EPS uplift = incremental revenue × operating contribution × after-tax conversion / shares

Operating contribution = 35%

After-tax conversion = 80%

Share count = 10.39M

| Incremental U.S. cosmetics revenue | EPS uplift | % of 2026F EPS |

|---|---|---|

| KRW 10B | +KRW 269 | +1.4% |

| KRW 30B | +KRW 808 | +4.1% |

| KRW 50B | +KRW 1,347 | +6.8% |

| KRW 100B | +KRW 2,695 | +13.6% |

KRW 10B alone does not move the stock. KRW 30B-50B begins to matter. At that point the story is no longer “cosmetics filled the medical-device gap.” It becomes “Rejuran brand equity can travel into consumer skincare.”

Margins are the test. If consolidated OPM stays near 38-40% while cosmetics grows, the market will stop treating cosmetics as lower-quality revenue. If growth is mostly promotion and channel spend, the re-rating stops.

5. Re-Rating Scenarios

The reference price in the attached report is KRW 295,000 as of May 29, 2026. Using Kiwoom’s 2026F EPS of KRW 19,760, 2026F PER is roughly 14.9x.

2026F PER = 295,000 / 19,760 = 14.93x

2027F PER = 295,000 / 24,722 = 11.93x

Using 2026F EPS of KRW 19,760:

| Target PER | Implied Price | Upside vs KRW 295,000 |

|---|---|---|

| 15.0x | KRW 296,000 | +0.5% |

| 17.5x | KRW 346,000 | +17.2% |

| 20.0x | KRW 395,000 | +33.9% |

| 22.5x | KRW 445,000 | +50.8% |

| 25.0x | KRW 494,000 | +67.5% |

The 20x scenario is KRW 19,760 × 20 = KRW 395,200, rounded to KRW 395,000.

| Zone | Required Evidence | Interpretation |

|---|---|---|

| 15x | Current market level | Medical-device slowdown and cosmetics discount reflected |

| 17.5x | Export recovery plus continued cosmetics growth | Partial re-rating |

| 20x | U.S. SKU velocity converts into 2Q26 numbers | Realistic bull case |

| 22.5x | Repeat sales across Sephora / Olive Young / Amazon / TikTok Shop | Global derma-cosmetics platform case |

| 25x | APR-style K-beauty premium partially applied | Still early |

6. Strategy

View

Buy now, but only a first tranche.

The current price already reflects a lot of disappointment. Around 15x 2026F EPS looks low relative to PharmaResearch’s profitability, net-cash profile and cosmetics growth. But U.S. sell-through is still an early signal, so a full position is premature.

Add Conditions

Consider adding if at least two of the following happen:

- Two REJURAN SKUs stay in Olive Young U.S. Top 20 for more than two weeks.

- 2Q26 cosmetics exports exceed KRW 30B.

- Sephora U.S. reviews, sell-outs and re-stocking show repeat demand.

- 2Q26 medical-device exports recover QoQ from KRW 21.1B in 1Q26.

- Consolidated OPM stays above 38%.

Invalidation

Cut the re-rating thesis if at least two of the following happen:

- Core REJURAN SKUs fall out of Olive Young U.S. Top 20 and Sephora traction slows.

- 2Q26 cosmetics exports fail to exceed 1Q26’s KRW 26.9B.

- Medical-device exports fail to recover again in 2Q26.

- Cosmetics growth pushes OPM below 35%.

- 2026F EPS is revised below KRW 17,000.

7. Conclusion

PharmaResearch’s multiple fell for a reason. The market is no longer willing to pay 30x purely for the Rejuran medical-device monopoly story. The 4Q25 miss and 1Q26 medical-device export pause were real.

But the price now reflects much of that disappointment. Cosmetics is already 29% of revenue. If Rejuran Cosmetics proves repeat sell-through at Sephora and Olive Young U.S., PharmaResearch can be reclassified from “slowing medical-device name” into a K-beauty healthcare platform that extends Rejuran across procedures and consumer skincare.

This is not a full-position moment based on story alone. It is a first-tranche moment after disappointment has been priced and the first U.S. sell-through signal has appeared. The next proof points are 2Q26 cosmetics exports, Sephora / Olive Young re-orders and OPM durability.

Evidence Map

[Fact]

- PharmaResearch reported 1Q26 revenue of KRW 146.1B, operating profit of KRW 57.3B and OPM of 39.2%. (PharmaResearch)

- 1Q26 cosmetics revenue was KRW 42.2B, about 29% of revenue; cosmetics exports were KRW 26.9B. (PharmaResearch)

- Rejuran Cosmetics entered Sephora U.S. online and about 380 physical stores. (PharmaResearch)

- As checked on May 31, 2026, Olive Young U.S. ranked REJURAN Dual Effect Ampoule #2 and REJURAN Turnover Ampoule #7. (Olive Young US)

[Inference]

- Cosmetics is becoming a core growth axis rather than a side business.

- Multiple compression reflects damaged visibility and a weaker medical-device monopoly narrative.

- Olive Young U.S. rankings matter more as a SKU-velocity signal than as direct revenue.

- Incremental U.S. cosmetics revenue of KRW 30B-50B begins to support estimate upgrades and multiple expansion.

[Speculation]

- Rejuran Cosmetics may earn part of the global K-beauty premium currently attached to APR-like names.

- Consumer skincare awareness may feed back into demand for Rejuran procedures.

- A 20-22.5x PER re-rating is possible if 2Q26 proof points arrive.

[Blocked]

- Olive Young U.S. unit sales, revenue and inventory data.

- Store-level Sephora sell-through and re-order data.

- Pure U.S. contribution inside Rejuran cosmetics exports.

- Confirmed 2Q26 cosmetics exports and consolidated OPM.

Disclaimer: This note is for research and information purposes only and is not personalized investment advice.