Follow-up context: this note follows Sam-Ha-Ma parity, SK hynix vs Micron, and Samsung HBM4E 12-high sample. Related hubs: AI HBM hub, Korea Daily Market Hub, and Korean stocks for foreign investors.

TL;DR

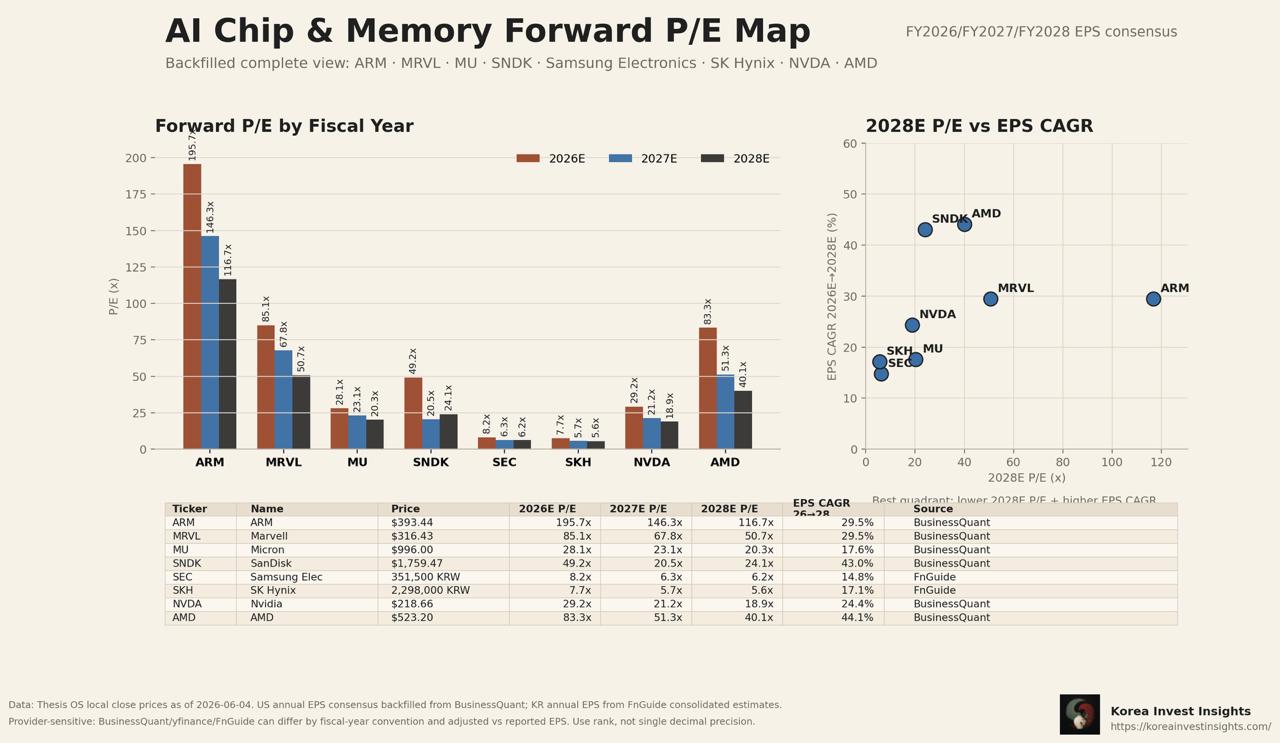

- This follow-up expands Sam-Ha-Ma from Samsung, SK hynix and Micron into a broader AI chip and memory forward P/E map including ARM, Marvell, NVIDIA, AMD and SanDisk.

- Samsung and SK hynix sit in the lowest P/E cluster of the AI chip basket. That is not automatically bullish. The market is still asking whether memory earnings are peak earnings.

- Micron deserves part of its premium: U.S. listing, dollar exposure, AI-memory scarcity, HBM4, SOCAMM2 and data-center SSD positioning all matter.

- But Samsung and SK hynix have not suffered an EPS breakdown. The relative discount is mostly the result of Micron re-rating first as the U.S. AI-memory proxy.

- Relative-value ranking remains: SK hynix first, Samsung as the larger HBM catch-up option, Micron as the benchmark rather than the cheapest stock.

AI Chip And Memory Map

The map uses Thesis OS local close prices and a mix of BusinessQuant and FnGuide EPS consensus. It should be read as a rank and cluster tool, not as a single-decimal absolute valuation model. Fiscal-year conventions, adjusted EPS definitions and source vendors differ across U.S. and Korean stocks.

| Ticker | 2026E P/E | 2027E P/E | 2028E P/E | 2026-2028 EPS CAGR | Read |

|---|---|---|---|---|---|

| ARM | 195.7x | 146.3x | 116.7x | 29.5% | Highest platform premium |

| MRVL | 85.1x | 67.8x | 50.7x | 29.5% | Custom silicon and networking premium |

| MU | 28.1x | 23.1x | 20.3x | 17.6% | U.S.-listed AI-memory proxy premium |

| SNDK | 49.2x | 20.5x | 24.1x | 43.0% | High-beta NAND/storage recovery |

| Samsung Electronics | 8.2x | 6.3x | 6.2x | 14.8% | Lowest large-cap AI-memory P/E cluster |

| SK hynix | 7.7x | 5.7x | 5.6x | 17.1% | HBM leader, still in the lowest P/E cluster |

| NVIDIA | 29.2x | 21.2x | 18.9x | 24.4% | Balanced growth and declining P/E |

| AMD | 83.3x | 51.3x | 40.1x | 44.1% | Strong growth expectation, high P/E |

The striking point is simple: Samsung and SK hynix are the lowest P/E names in this AI chip and memory basket.

That can mean either opportunity or a value trap. The key question is whether 2027-2028 EPS holds.

Micron Premium Is Not A Technology Premium

Micron is a very good company in this cycle. It also gives U.S. investors the cleanest large-cap memory proxy.

Micron guided FY3Q26 revenue to $33.5 billion, gross margin to about 81%, and non-GAAP diluted EPS to $19.15. (Micron IR) In its prepared remarks, Micron said it continues to expect DRAM and NAND supply-demand conditions to remain tight beyond calendar 2026. It also described very sharp sequential price increases in DRAM and NAND. (Micron Prepared Remarks)

That supports a premium.

But the premium should not be misread as HBM technology leadership over SK hynix. The cleaner interpretation is:

Micron premium

= U.S. listing premium

+ AI-memory scarcity premium

+ dollar asset premium

+ HBM4 / SOCAMM2 / data-center SSD platform narrative

+ strong FQ3 guidance

Korean Memory Discount Looks Too Wide

Korean memory also deserves some discount.

Samsung is not a pure memory company. It carries smartphones, appliances, displays, foundry and system LSI. It also still has an HBM catch-up discount.

SK hynix is cleaner, but it is still a Korean-listed, won-denominated stock with foreign-access and Korea-discount friction.

Even so, the discount looks wide.

Using the user-provided local run-rate operating profit snapshot:

| Company | Earnings base | Annualized OP | Equity value / market cap | Run-rate OP multiple |

|---|---|---|---|---|

| Samsung Electronics | 2Q26E OP about KRW 90tn | about KRW 360tn | about KRW 2,176tn | about 6.0x |

| SK hynix | 2Q26E OP about KRW 66.5tn | about KRW 266tn | about KRW 1,532tn | about 5.8x |

| Micron | FY3Q26 OP about $25.7bn | about $102.8bn | about $1.137tn | about 11.1x |

Micron trades at roughly 1.8-1.9x the Korean memory run-rate operating-profit multiple. Some U.S. premium is fair. But that spread is hard to justify if SK hynix remains the HBM leader and EPS estimates stay intact.

Stock Read

SK hynix

SK hynix is the clearest relative-value name. It has the most visible HBM leadership, a 2028E P/E of 5.6x, and a 2026-2028 EPS CAGR of 17.1%, close to Micron’s 17.6% in the map.

The buy case is not “memory is cheap” in a generic sense. It is that the HBM leader trades at a deeper discount than the U.S. AI-memory proxy should command.

The caveat is flow. Full sizing needs foreign selling to slow, 2Q earnings to confirm the run-rate, and 3Q DRAM/HBM price guidance to hold.

Samsung Electronics

Samsung’s discount is more justified than SK hynix’s discount. It is a conglomerate-like technology platform, not a memory pure-play, and HBM credibility is still being rebuilt.

But the upside path is still meaningful. Samsung does not need to trade at Micron’s multiple. A move from roughly 6x run-rate OP to 7-8x would already matter if HBM4E qualification and DS earnings momentum improve.

Micron

Micron remains the benchmark. It is the U.S.-listed AI-memory proxy and has strong near-term numbers. But after the re-rating, it is no longer the cheapest relative-value expression of the same memory cycle.

Bottom Line

Micron deserves a premium. But the Korean memory discount has likely gone too far if EPS durability holds.

The practical ranking is:

1. SK hynix

- HBM leader

- lowest P/E cluster

- excessive discount versus Micron

2. Samsung Electronics

- more justified discount

- larger HBM catch-up option

3. Micron

- high-quality benchmark

- less relative upside after re-rating

In one sentence:

Memory stocks look cheap again not because earnings collapsed, but because the U.S. AI-memory proxy got expensive first. As long as that gap remains, the Sam-Ha-Ma parity trade is still alive.

Sources And Data

- AI Chip & Memory Forward P/E Map: Thesis OS local close prices plus BusinessQuant and FnGuide consensus, as of June 4, 2026.

- Micron FY2Q26 results and FY3Q26 guidance: Micron IR

- Micron FY2Q26 prepared remarks: Micron Prepared Remarks

- Prior notes: Sam-Ha-Ma parity, SK hynix vs Micron