Follow-up context: this note follows Samsung vs SK hynix forward PER inversion, SK hynix vs Micron, and Samsung HBM4E 12-high sample. Related hubs: AI HBM hub, Korea Daily Market Hub, and Korean stocks for foreign investors.

TL;DR

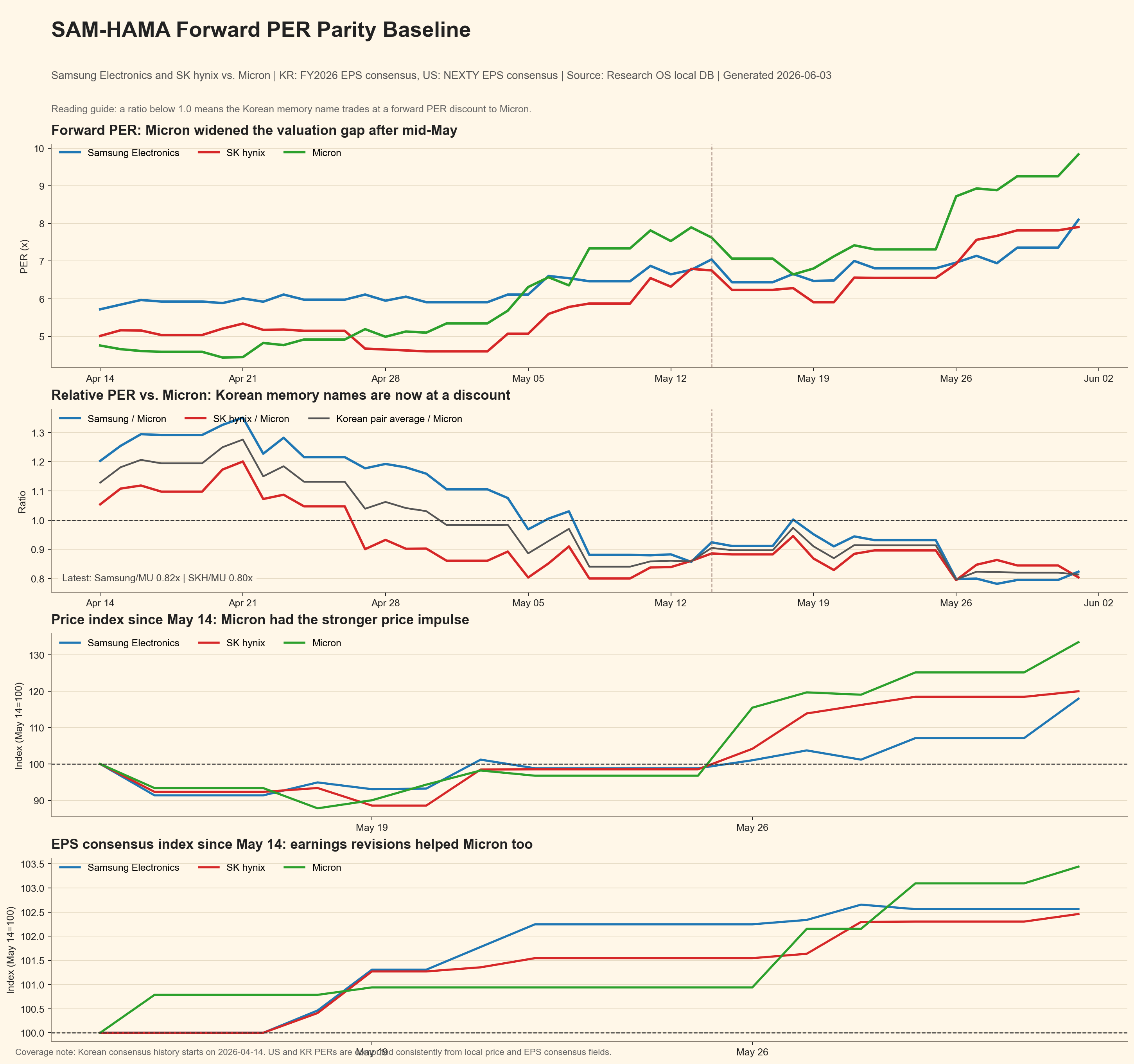

- The relative discount since mid-May is not about a deterioration in Samsung or SK hynix. It is mostly about Micron re-rating faster.

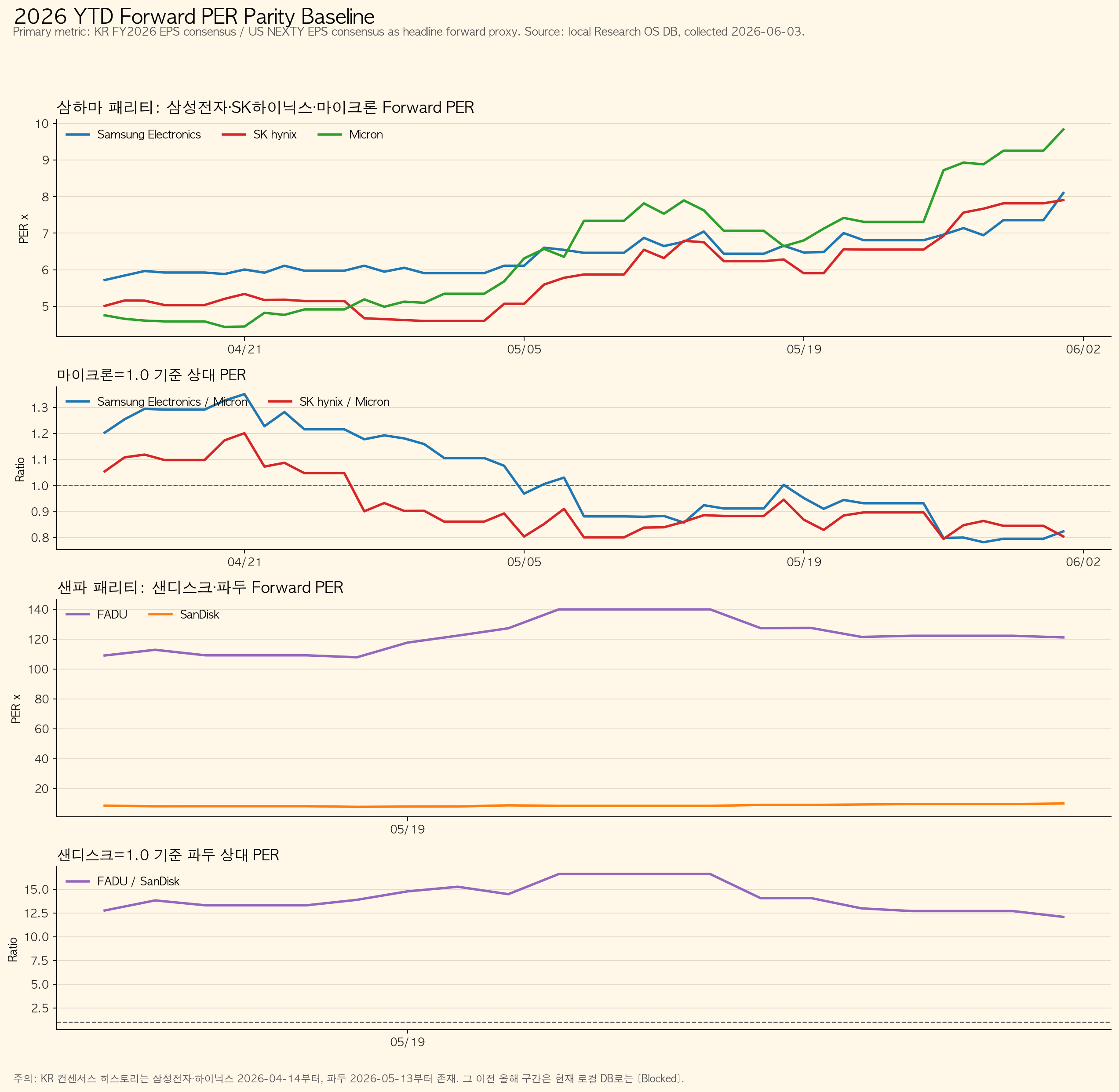

- As of June 1, 2026, Samsung/Micron forward PER is 0.82x and SK hynix/Micron is 0.80x.

- Samsung is now roughly 20% below its Samsung/Micron average ratio of 1.03x. SK hynix is roughly 13% below its SK hynix/Micron average ratio of 0.93x.

- SK hynix is buyable on a first tranche from a relative-value angle, but foreign selling still argues for scaling in.

- Samsung has a larger catch-up path if HBM4E/HBM4 credibility and foreign flow improve.

Forward PER Parity

| Name | Latest forward PER | Period average PER | Latest vs Micron | Average vs Micron |

|---|---|---|---|---|

| Samsung Electronics | 8.10x | 6.43x | 0.82x | 1.03x |

| SK hynix | 7.90x | 5.87x | 0.80x | 0.93x |

| Micron | 9.84x | 6.49x | 1.00x | 1.00x |

Data basis: Research OS local DB, KR FY2026 EPS for Samsung and SK hynix, US NEXTY EPS for Micron, 49 trading days from April 14 to June 1, 2026. Download: daily panel CSV, baseline summary CSV.

What Changed Since Mid-May

| Name | May 14 PER | June 1 PER | Change |

|---|---|---|---|

| Micron | 7.62x | 9.84x | +29.0% |

| SK hynix | 6.75x | 7.90x | +17.1% |

| Samsung Electronics | 7.04x | 8.10x | +15.0% |

Micron’s price rose faster than Korean memory leaders while all three saw EPS estimates improve. That makes the current discount a relative-value gap, not an earnings-damage signal.

Investment Read

SK hynix remains the cleaner HBM leader. At 0.80x Micron, a return to the 0.89x mid-May ratio implies roughly 10% multiple catch-up; a return to the 0.93x post-April average implies roughly 15%.

Samsung is less proven in HBM, but the relative discount is larger. If Samsung returns to its average Samsung/Micron ratio of 1.03x while Micron’s PER holds near 9.84x, Samsung’s implied relative PER is about 10.1x versus the current 8.1x. That is a multiple catch-up path, not a price target.

The main risks are a Micron derating, Samsung HBM qualification delay, persistent foreign selling in Korea, and EPS downgrades.

Bottom Line

SK hynix is the memory leader that is already buyable in a first tranche. Samsung is the larger catch-up candidate if HBM credibility improves. The common condition for sizing up is foreign-flow stabilization.

Sources: Micron FY2Q26 results, Micron prepared remarks.