📚 Context This is a deeper CPI companion to CPI, BOJ and FOMC: Korea Needs a Reaction Function, Not a Forecast. That note framed the macro event cluster. This one focuses on the first gate: U.S. May CPI itself. Related reading: the jobs shock and the KOSPI 8,000 gate, the AI supercycle midgame and rate risk and the complex risk-off recovery map.

TL;DR

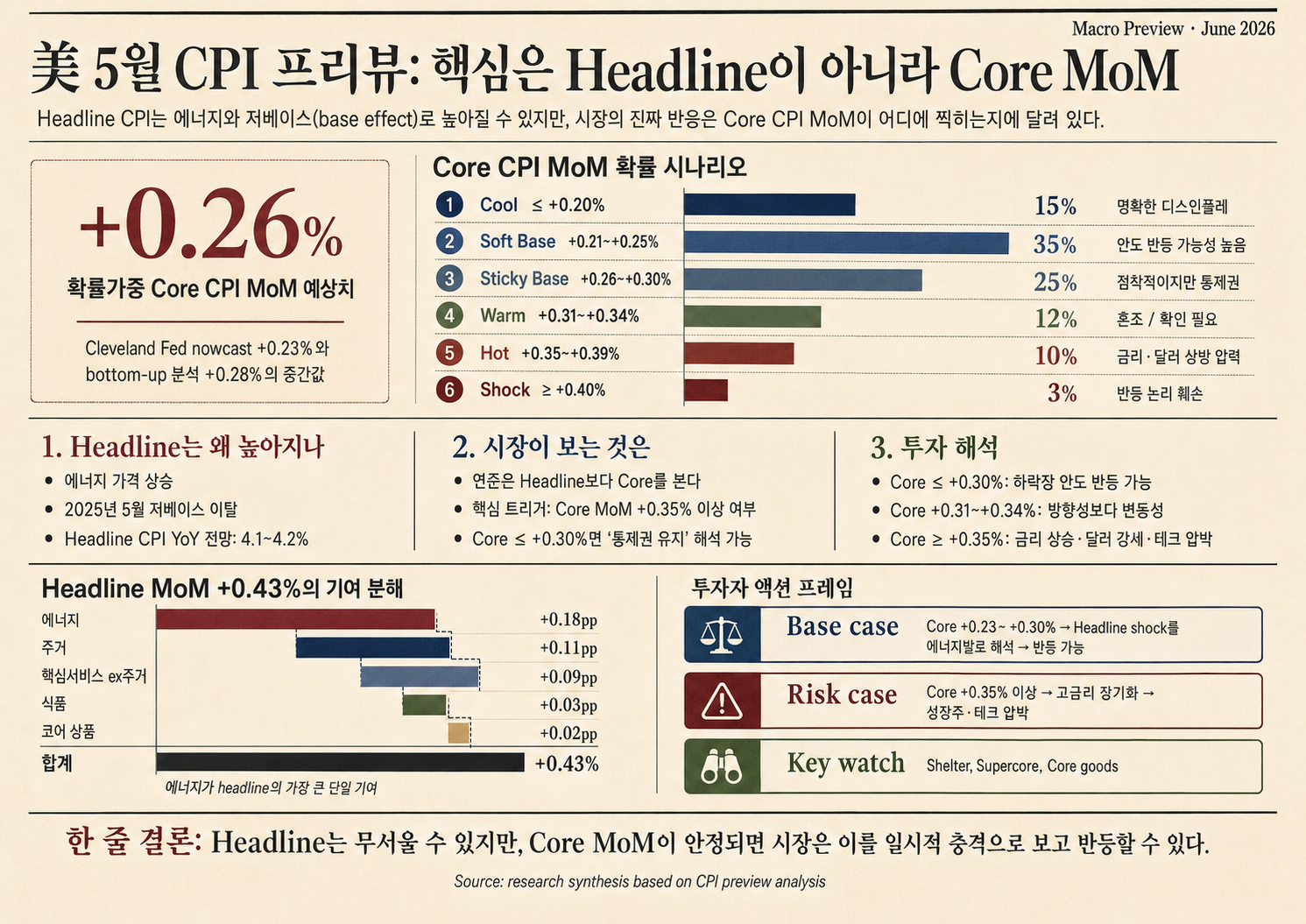

- Headline CPI is likely to look hot. Energy prices and the low May 2025 base both work upward. The central range is Headline CPI +0.43-0.46% MoM / 4.1-4.2% YoY.

- The key market variable is core CPI MoM, not headline CPI. Cleveland Fed’s June 5 nowcast puts May 2026 core CPI at +0.23% MoM / 2.82% YoY. Combining that with the bottom-up proxy of +0.28%, the probability-weighted center is Core CPI MoM +0.26%. (Cleveland Fed)

- The neutral probability distribution leans toward relief, but only conditionally. I put the probability of Core CPI MoM at +0.30% or lower at 75%, and the probability of a +0.35% or higher hot print at 13%. That means a relief bounce is the base case, but defense should start immediately above +0.35%.

- U.S. and Korean equity investors need to separate rate-sensitive growth from energy, quality cash-flow and dollar beneficiaries. For Korean investors, the key is to separate KRW weakness protection, semiconductor multiple risk, and cost pass-through in refining, airlines, chemicals and utilities.

1. Scope

The source research is a pre-release, proxy-based CPI nowcasting note. It argued that May CPI could beat market expectations because of energy and base effects. The original range was headline CPI 4.1-4.2% YoY, core CPI 2.9-3.0% YoY, headline MoM +0.4-0.5%, and core MoM around +0.3%.

This blog version keeps the data-rich structure but reframes the investment decision around five questions.

| Question | Why it matters |

|---|---|

| Is the surprise point headline or core? | A hot headline caused by energy may not be enough to force a Fed repricing. |

| How much do energy and the May 2025 base lift YoY CPI? | YoY acceleration can be mechanical, not structural. |

| Is core CPI at 3.0% YoY a base case or a hot scenario? | Cleveland Fed nowcast suggests 3.0% is the upper-risk case, not the center. |

| How does CPI feed into FOMC, rates, USD and risk assets? | CPI arrives just before the June FOMC. |

| How should U.S. and Korean investors adjust sector, style and FX exposure? | Korea receives CPI through both rates/FX and energy-cost channels. |

[Fact] The BLS release schedule sets May 2026 CPI for June 10, 2026 at 8:30 a.m. ET, or 21:30 KST. (BLS CPI Schedule)

2. What To Keep And What To Lower

| Item | Refined view |

|---|---|

| Nature of note | A pre-release CPI nowcast, not an official forecast. |

| Strength | Correctly identifies energy, the May 2025 low base and the April CPI structure. |

| Weakness | The “core 3.0% YoY” framing is aggressive relative to Cleveland Fed nowcast. |

| Final framing | Keep headline upside; lower core upside to conditional; make Core MoM trigger the investment framework. |

The central distinction is simple: a high headline is likely; a dangerous core is not yet confirmed.

3. Key Facts

April baseline: BLS reported April 2026 headline CPI at +0.6% MoM SA / +3.8% YoY NSA and core CPI at +0.4% MoM / +2.8% YoY. Energy rose +3.8% MoM, gasoline +5.4%, shelter +0.6%, and airline fares +2.8%. (BLS CPI Summary)

Low base: May 2025 headline and core CPI both rose just +0.1% MoM SA. That makes May 2026 YoY inflation mechanically easier to lift. (BLS May 2025 CPI)

Gasoline proxy: EIA weekly regular gasoline prices averaged roughly $4.103/gal in April and $4.479/gal in May.

4.479 / 4.103 - 1 = +9.2%

That supports headline upside, although the June 1 price fell to $4.305/gal, which could reverse some pressure for June CPI. (EIA)

4. Refined Core CPI MoM Probability Distribution

Headline is likely to look hot because of energy and base effects. The equity event is core. This distribution combines the Cleveland Fed nowcast of +0.23%, the bottom-up weighted proxy of +0.28%, and the upside risk from April’s core acceleration.

| Scenario | Core CPI MoM | Probability | Market interpretation | Equity reaction |

|---|---|---|---|---|

| Cool | ≤ +0.20% | 15% | Clear disinflation | Strong relief bounce |

| Soft Base | +0.21-0.25% | 35% | In line with Cleveland nowcast | High probability of rebound |

| Sticky Base | +0.26-0.30% | 25% | Sticky but controlled | Possible bounce after initial dip |

| Warm | +0.31-0.34% | 12% | Ambiguous; rate pressure remains | Limited rebound or mixed tape |

| Hot | +0.35-0.39% | 10% | Second-round effects | Growth and tech pressure |

| Shock | ≥ +0.40% | 3% | Repeat of April acceleration | Bounce fails; yields and USD rise |

EV = Σ(scenario probability × interval midpoint) ≈ +0.26%

In compact form:

| Core CPI MoM range | Probability | Investment read |

|---|---|---|

| +0.30% or lower | 75% | Headline shock can be treated as energy/base effect. Relief bounce possible. |

| +0.31-0.34% | 12% | Ambiguous. A rebound may be limited. |

| +0.35% or higher | 13% | Risk. Higher yields, stronger USD and tech valuation pressure return. |

5. Weight-Based Sanity Check

BLS April 2026 relative-importance weights were energy 7.090%, food 13.560%, core CPI 79.351%, commodities less food and energy 19.002%, and shelter 35.320%. (BLS CPI Table 1)

Using the source report’s component assumptions:

Headline CPI MoM proxy

= 0.07090 × 2.8

+ 0.13560 × 0.2

+ 0.19002 × 0.1

+ 0.35320 × 0.32

+ 0.25028 × 0.35

= 0.445% ≈ +0.45%

For core:

Core CPI MoM proxy

= (0.19002 × 0.1 + 0.35320 × 0.32 + 0.25028 × 0.35) / 0.79351

= 0.277% ≈ +0.28%

This supports a headline range near +0.43-0.46% and a bottom-up core proxy near +0.28%. Cleveland Fed’s +0.23% nowcast pulls the probability-weighted center toward +0.26%. Therefore, core at +0.35% or above is a defensive tail scenario, not the base case.

6. Transmission Map

| CPI component | First market reaction | Second data point | Investment interpretation |

|---|---|---|---|

| Energy CPI upside | Headline shock; energy-sensitive sectors move | Gasoline, crude, diesel, airline fuel | Not necessarily enough for immediate Fed repricing. |

| Shelter normalization | Core MoM stays contained | Rent, OER, lodging away from home | Core +0.25-0.30% can be equity-relief territory. |

| Supercore reacceleration | Long yields higher, USD stronger, growth pressured | Airfares, insurance, medical services | Core +0.35-0.40%+ means hawkish repricing risk. |

| PPI follow-through | Margin and pass-through risk | June 11 PPI | April PPI was already hot; another hot PPI can erase CPI relief. |

[Fact] April 2026 PPI final demand rose +1.4% MoM / +6.0% YoY. (BLS PPI)

7. U.S. Equity Playbook

| CPI result | U.S. market read | Portfolio action |

|---|---|---|

| Core MoM ≤ +0.25% | Headline is energy; core is stable. | Quality growth, select semis and duration risk can recover. |

| Core MoM +0.26-0.30% | Sticky but controlled. | Dip-then-bounce possible; confirm yield reversal. |

| Core MoM +0.31-0.34% | Ambiguous. | Wait for PPI and FOMC; keep a quality bias. |

| Core MoM ≥ +0.35% | Second-round effects. | Reduce high-multiple growth, small caps and REITs; prefer energy, quality cash flow and defensives. |

| Core MoM ≥ +0.40% with shelter/supercore | Fed repricing. | Cut beta; hold more cash, short duration and USD exposure. |

8. Korea Equity Playbook

Korea receives U.S. CPI through two channels.

| Channel | Path |

|---|---|

| Rates and FX | Hot core CPI → higher U.S. yields → stronger USD / weaker KRW → potential foreign-flow pressure. |

| Real cost | Higher energy → Korean import-price and margin pressure → airlines, chemicals, utilities and transport under pressure. |

| Korean style / sector | Hot CPI impact | Cool CPI impact |

|---|---|---|

| Semiconductors / AI supply chain | KRW weakness helps translation, but U.S. tech multiple pressure can dominate near term. | Growth relief and foreign-flow recovery. |

| Autos / shipbuilding / machinery | Weak KRW helps exporters, but U.S. demand and input costs matter. | FX stabilizes and demand worries ease. |

| Batteries / internet / biotech | Vulnerable to discount-rate pressure. | Rate relief can support rebound. |

| Refining | Potential relative beneficiary from energy prices. | Momentum fades if gasoline/oil cool. |

| Chemicals / airlines / utilities | Cost pressure. | Cost relief. |

| Banks / insurance | Mixed: rates help some income lines, but credit and KRW risks matter. | More nuanced; depends on curve and credit. |

For Korean investors holding U.S. stocks, the key is to separate equity beta from FX hedge ratio. Hot CPI can hurt U.S. equities but also strengthen USD, cushioning unhedged positions in KRW terms.

9. Immediate Checklist

| Priority | Item | Threshold |

|---|---|---|

| 1 | Core CPI MoM | ≤0.25% relief; +0.26-0.30% controlled; +0.31-0.34% ambiguous; ≥0.35% risk; ≥0.40% hawkish shock. |

| 2 | Shelter / OER / Rent | Around 0.3% is relief; ≥0.5% is core stickiness. |

| 3 | Supercore | Airfares, insurance and medical services. |

| 4 | Core goods | Apparel, furnishings and vehicles indicate tariff pass-through risk. |

| 5 | Energy CPI | Explains headline; not the core Fed trigger. |

| 6 | June 11 PPI | Hot PPI can weaken CPI relief. |

| 7 | June 16-17 FOMC | Watch SEP and inflation-expectations language. |

Final Take

Headline CPI at 4.1-4.2% is a plausible base case. That alone is not enough to aggressively cut risk. The probability-weighted center is Core CPI MoM +0.26%, the probability of +0.30% or lower is 75%, and the probability of a +0.35% or higher hot print is 13%. The base case is a possible relief bounce. Defense begins above +0.35%.

For U.S. equities, this is a factor-rotation event. For Korean equities, it is both a rates/FX event and an energy-cost event. Base case means volatility, not a structural sell signal, and a recent sell-off could rebound if core stays at +0.30% or lower. Hot case means higher U.S. yields, stronger USD and weaker KRW can arrive together, so Korean investors should be more selective in semis, internet and batteries while watching relative defense in refining, quality exporters and USD cash.

Evidence Classification

[Fact]

- May 2026 CPI is scheduled for June 10, 2026 at 8:30 ET. (BLS CPI Schedule)

- Cleveland Fed June 5 nowcast puts May CPI at +0.46% MoM / 4.18% YoY and core CPI at +0.23% MoM / 2.82% YoY. (Cleveland Fed)

- April 2026 CPI was headline +0.6% MoM / +3.8% YoY and core +0.4% MoM / +2.8% YoY. (BLS CPI Summary)

- April 2026 PPI final demand was +1.4% MoM / +6.0% YoY. (BLS PPI)

- The April FOMC kept the target range at 3.50-3.75%. (Federal Reserve)

[Inference]

- Headline upside is likely, but much of it is energy and base effect.

- The probability-weighted center for Core CPI MoM is +0.26%, with +0.30% or lower at 75% probability and +0.35% or higher at 13% probability.

- Core CPI MoM above +0.35% is the real risk-asset trigger.

- Korea’s response will be sector-specific because KRW weakness can help exporters while higher global discount rates hurt high-multiple growth.

[Blocked]

- Actual May CPI, May PPI and June FOMC SEP are not yet released.

- This is a pre-release event framework; it needs updating immediately after the CPI print.