Bản đồ cô đọng cho luận điểm catch-up của Samsung Electronics qua cổ phiếu thường, cổ phiếu ưu đãi và Samsung C&T.

Cách thể hiện giao dịch catch-up của Samsung Electronics

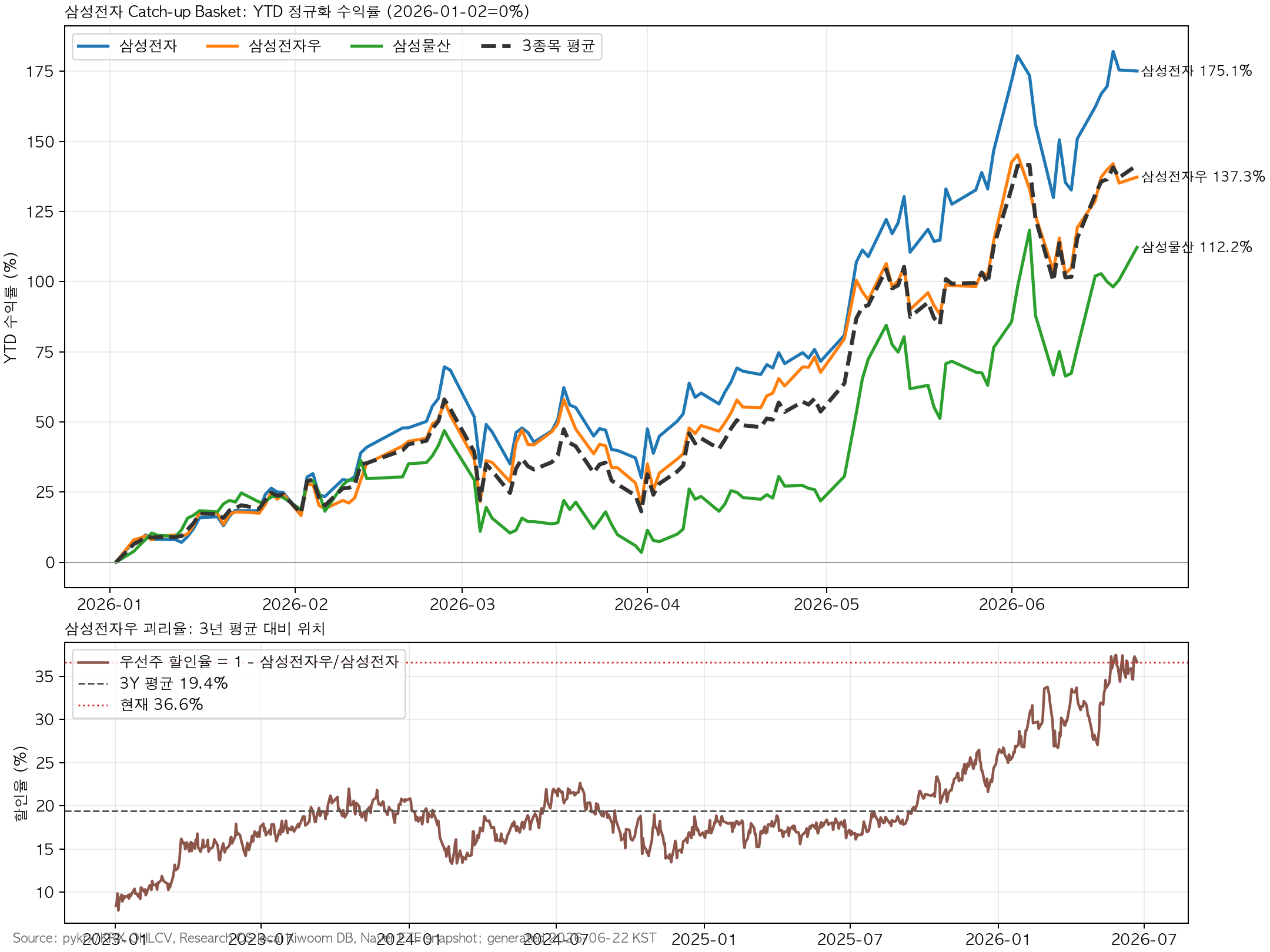

Cổ phiếu thường Samsung Electronics đã tăng mạnh nhờ HBM, chu kỳ bộ nhớ và kỳ vọng hoàn trả dòng tiền tự do. Câu hỏi là nên thể hiện cùng một luận điểm bằng cổ phiếu thường, cổ phiếu ưu đãi hay Samsung C&T.

Tóm tắt

Samsung Electronics preferred is the cleaner catch-up expression. It lagged the common by 37.8 percentage points YTD and traded at a 36.6% discount on 22 June 2026.

The discount is extreme: 36.6% versus a 19.4% three-year average, 18.1% median, +3.11 z-score, and 99.1st percentile.

Samsung C&T is not a one-for-one Samsung Electronics proxy. It is a NAV and affiliate-dividend story.

ETF cap spillover is secondary. A simple redistribution assumption implies only about KRW 24.6bn into Samsung Electronics preferred and KRW 46.0bn into Samsung C&T.

Dữ liệu chính

Stock

2 Jan Close

22 Jun Close

YTD

Versus Samsung Electronics

Samsung Electronics

KRW 128,500

KRW 353,500

+175.1%

Baseline

Samsung Electronics preferred

KRW 94,400

KRW 224,000

+137.3%

-37.8pp

Samsung C&T

KRW 245,000

KRW 520,000

+112.2%

-62.9pp

Metric

Samsung Electronics

Samsung Electronics Preferred

Samsung C&T

20D return

+18.0%

+19.3%

+24.3%

60D return

+86.3%

+67.0%

+84.7%

Correlation with Samsung Electronics

1.000

0.949

0.779

Beta to Samsung Electronics

1.000

0.912

0.848

Chiết khấu cổ phiếu ưu đãi

Metric

Value

Preferred/common ratio

63.37%

Current discount

36.63%

Three-year average discount

19.43%

Three-year median discount

18.14%

Current z-score

+3.11

Three-year percentile

99.1%

Preferred/Common Ratio

Implied Preferred Price

Upside

Current 63.4%

KRW 224,000

Baseline

70.0%

KRW 247,450

+10.5%

75.0%

KRW 265,125

+18.4%

80.0%

KRW 282,800

+26.3%

85.0%

KRW 300,475

+34.1%

NAV của Samsung C&T

Samsung C&T is calculated to hold 298,818,100 Samsung Electronics shares. At KRW 353,500, that stake is worth about KRW 105.6tn. Samsung C&T’s estimated market cap is about KRW 84.3tn.

Foreign selling slows, program selling eases, 20-day moving average holds

The key conclusion is that the next Samsung Electronics catch-up alpha is more likely to come from preferred-share discount normalization than from ETF cap spillover.